Establishment of the National Grain Exchange

February 22, 1908 Establishment of the National Grain Exchange

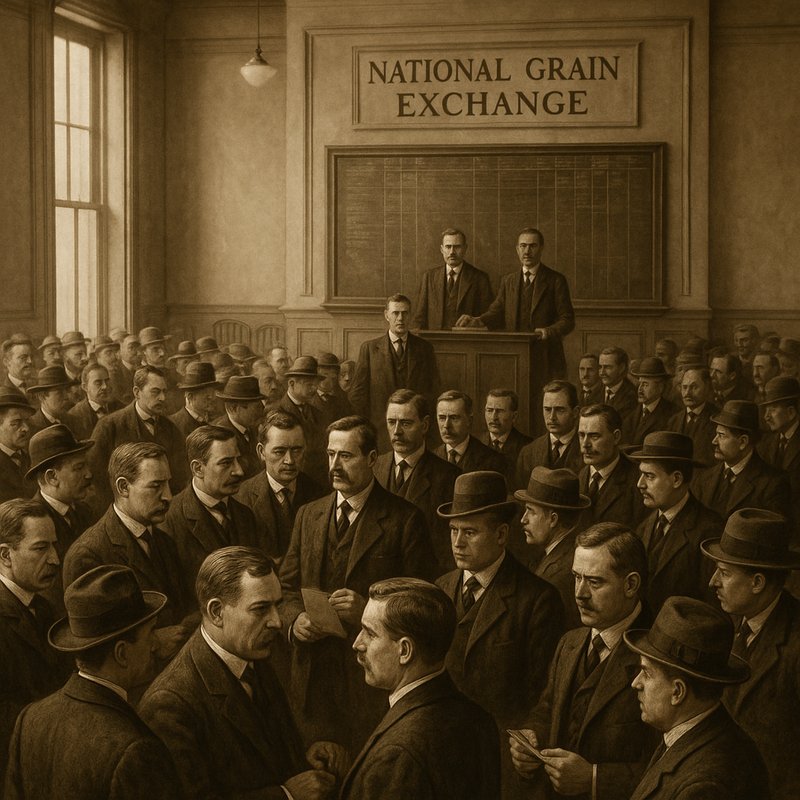

On February 22, 1908, you can trace the moment grain trading stopped being a chaotic, fraud-ridden system and became a regulated market. The National Grain Exchange formalized standardized contracts, uniform grading rules, and mandatory price reporting that day. It replaced informal networks where brokers manipulated terms and graders cheated farmers. That single institutional shift reshaped how wheat moved from prairie settlements to national markets — and its influence runs deeper than most traders realize.

Key Takeaways

- The National Grain Exchange was formally established on February 22, 1908, marking a pivotal moment in organized commodity trading in the United States.

- Its primary purpose was to standardize commodity contracts and grading systems, creating transparency and accountability across regional grain markets.

- The Exchange emerged in response to widespread fraud, including wheat adulteration, grader manipulation, and broker misrepresentation that eroded market confidence.

- February 22, 1908 crystallized mounting pressures from regulatory neglect, market manipulation, and rapid prairie expansion straining informal trading mechanisms.

- The Exchange redefined grain commerce by replacing informal trading networks with defined rules governing price formation, participation, and contract transparency.

What Was the National Grain Exchange and Who Created It?

The National Grain Exchange, established on February 22, 1908, emerged during a pivotal era when organized commodity trading in the United States was rapidly maturing and drawing increasing federal scrutiny. You'll find that its origins carry founding myths, with competing accounts disputing whether it represented a newly chartered national institution or a reorganized regional body.

Membership disputes further clouded its early identity, as grain merchants, brokers, and speculators each claimed stakes in shaping its governance. What's clear is that the exchange arose within a broader landscape already anchored by powerhouses like the Minneapolis Chamber of Commerce and the Chicago Board of Trade.

Understanding who created it requires separating documented records from retrospective narratives that often blurred lines between local ambition and national scope.

The Wheat Market Scandals That Made 1908 a Breaking Point

Wheat market scandals didn't just create pressure for reform in 1908—they made organized exchange governance feel like an urgent necessity rather than a regulatory luxury. You'd find that wheat adulteration had become widespread enough to erode buyer confidence across regional and national markets. Farmers received unfair prices because graders manipulated quality classifications, and broker fraud compounded losses by misrepresenting transaction terms to unsuspecting clients.

Federal investigators were already scrutinizing futures trading practices, and their findings exposed how easily unregulated intermediaries could exploit pricing systems. These abuses pushed stakeholders—traders, farmers, and legislators—toward demanding structured oversight. The scandals of this era didn't simply embarrass the industry; they demonstrated that informal self-regulation had failed and that a formal institutional response was no longer optional. The rapid influx of settlers drawn by the Dominion Lands Act had dramatically expanded prairie wheat production, flooding markets with volume that existing informal trading mechanisms were wholly unprepared to manage with any consistency or fairness.

Why February 22, 1908 Changed Grain Trading Forever

February 22, 1908 didn't arrive quietly in the grain trading world—it crystallized years of fraud, manipulation, and regulatory neglect into a single institutional reckoning. You can trace its cultural impact through the shift in how traders, farmers, and lawmakers talked about commodity markets.

Speculative narratives that once glorified bold market plays gave way to demands for transparency and accountability. The establishment of a formalized grain exchange on this date forced participants to operate within defined rules rather than personal networks and backroom deals.

You're looking at a moment when institutional structure replaced informal power. That evolution didn't just clean up trading floors—it redefined who could participate, how prices formed, and what grain commerce meant to the broader American economy. The grain being traded increasingly originated from prairie homestead settlements that had expanded rapidly under the Dominion Lands Act, which offered 160 free acres to settlers willing to meet five-year residency and improvement requirements.

Minneapolis, Chicago, and the Battle for Grain Market Control

Institutional reform doesn't happen in a vacuum—it happens because competing power centers force each other's hands. By 1908, Minneapolis and Chicago weren't cooperating—they were competing. Chicago's Board of Trade held enormous leverage through its rail connections, controlling how grain moved east and how prices got reported nationally. Minneapolis pushed back by developing its own price signaling infrastructure, broadcasting hard red spring wheat valuations that Chicago couldn't ignore.

You can trace federal regulatory pressure directly to this rivalry. When two major markets price the same commodity differently, traders exploit the gap, and instability follows. Washington noticed. The friction between these cities didn't just reshape regional commerce—it forced national conversations about standardization, transparency, and accountability that ultimately produced the regulatory frameworks governing grain futures trading today. This same tension between regional market authority and federal oversight echoed the legal battles over interstate commerce regulation that emerged from steamboat monopoly disputes nearly a century earlier.

How the National Grain Exchange's Buildings Signaled Market Dominance

Architecture doesn't lie. When you walk past the Minneapolis Grain Exchange's Main Building, you immediately read power in its steel-framed ten-story shell. Kees and Coburn designed it in the Chicago Commercial style, embedding architectural symbolism directly into the structure—wheat shafts and corn ears carved into the façade told competitors exactly what this institution controlled.

These buildings weren't decorative. They enforced trading rituals and institutional authority through physical permanence:

- The Main Building (1902–1903) established structural dominance with one of Minneapolis's first steel frames

- The East Building (1909) expanded trading capacity as market volume surged

- The North Building (1928) replaced the original 1884 exchange site

- Decorative grain motifs connected every transaction to commodity identity

Stone and steel made market dominance undeniable. Much like the international standardization of water polo rules by FINA in 1911 brought order to a previously fragmented sport, the Exchange's physical consolidation imposed unified institutional authority over a commodity market that had long operated without consistent oversight.

The Grading and Pricing Rules the National Grain Exchange Forced Into Practice

Standardization was the mechanism the National Grain Exchange wielded to transform chaotic local pricing into a disciplined national system. Before 1908, you'd encounter wildly inconsistent grading standards across regional markets, making fair valuation nearly impossible. Buyers and sellers couldn't trust quotes from distant markets because no uniform classification existed for moisture content, weight, or purity.

The Exchange forced grading standards onto reluctant traders by tying market access to compliance. You couldn't participate in futures contracts without submitting grain to certified inspectors who applied consistent criteria. That requirement created pricing transparency almost immediately. Once every bushel carried a recognized grade, published prices meant the same thing in Minneapolis as they did in Chicago. Uniform grading didn't just reduce disputes—it built the trust that made national commodity trading viable. The same principle of standardized coordination appeared in disaster relief efforts, where the Halifax Relief Committee demonstrated that consistent distribution protocols prevented duplication and ensured aid reached survivors equitably regardless of religious affiliation.

How Federal Pressure Reshaped the National Grain Exchange's Authority

Federal investigators didn't arrive to celebrate what the National Grain Exchange had built—they arrived to dismantle the parts that served private interests over public ones. Federal oversight forced the exchange to rethink who it actually served.

Key pressure points that reshaped authority included:

- Grading audits that exposed inconsistent standards benefiting insiders

- Market consolidation reviews revealing price manipulation across regional exchanges

- Mandatory reporting requirements limiting secretive trading arrangements

- Contract transparency rules that stripped brokers of unchecked discretionary power

You can trace today's commodity regulations directly to this friction. Federal agencies didn't just critique the exchange—they restructured it.

What had functioned as a private club operating public markets now answered to external authority, fundamentally shifting where power over grain pricing actually resided. Similar tensions between individual interests and community protection shaped Canada's 2005 reforms to criminal justice procedures, which restructured how courts and review boards handled accused persons with serious mental health issues.

How the National Grain Exchange Still Shapes Commodity Markets Today

What the National Grain Exchange put in motion over a century ago still runs beneath every bushel traded today. You can trace modern contract standardization, price transparency, and market oversight directly back to the structural decisions made in 1908.

Even algorithmic trading systems rely on the pricing benchmarks and grading protocols that early exchanges formalized. Without that foundation, automated strategies would have no reliable data to act on.

Climate risk has also forced today's commodity markets to revisit the Exchange's original logic: when weather disrupts supply, standardized contracts keep trading orderly rather than chaotic. You're fundamentally working within a system those early architects designed to absorb uncertainty. Their framework didn't just survive modernization—it quietly made modernization possible.

The same principle of building on existing infrastructure rather than starting from scratch is visible today in ventures like Axiom Space, where attaching to the ISS allowed the company to leverage existing power and life-support systems instead of rebuilding them at enormous cost.