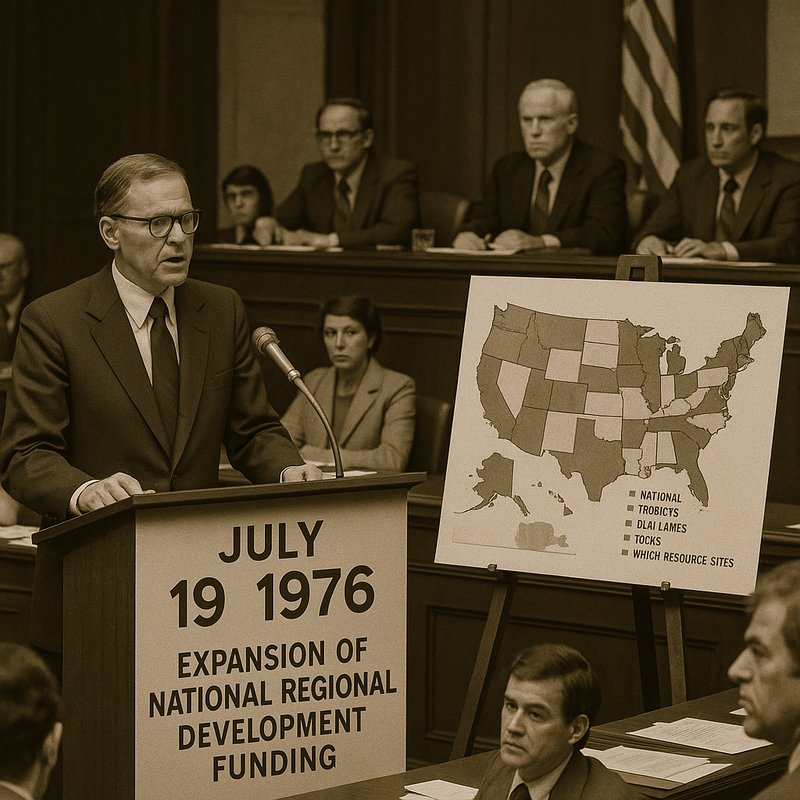

Expansion of National Regional Development Funding

July 19, 1976 Expansion of National Regional Development Funding

On July 19, 1976, you'll find Congress didn't simply expand regional development funding — it restructured how the federal government compensates counties that permanently lose property tax revenue when federal agencies acquire land. Counties across the West had watched their tax bases shrink while service obligations stayed the same. The new framework established formula-driven, entitlement-based payments covering national forests, BLM lands, parks, and water resource sites — costing roughly $117 million annually. There's much more to uncover about how this landmark policy works.

Key Takeaways

- July 1976 proposals established formula-driven federal payments to counties burdened by large, untaxable federal land holdings across the nation.

- The entitlement framework covered National Parks, National Forests, BLM lands, and water-resource sites, excluding military bases.

- Payment formulas capped compensation at $0.10 per acre or $0.05 per acre minus other federal aid, whichever was greater.

- Recently acquired National Park or Wilderness lands triggered a separate calculation: 1% of fair market value paid annually.

- The Office of Management and Budget estimated the program's annual cost at roughly $117 million, signaling substantial nationwide fiscal commitment.

The 1976 Campaign to Compensate Federal Land Counties

By the mid-1970s, counties hosting large federal land holdings had grown increasingly frustrated with shrinking tax bases they couldn't control. When federal agencies acquired private land, local governments lost property-tax revenue but kept their service obligations. You can see how this shaped the rural political economy of western states, where federal ownership dominated entire counties.

Community advocacy intensified as local officials pushed Congress to recognize this imbalance as a structural problem, not a temporary inconvenience. By July 1976, legislators were advancing proposals to authorize direct payments to affected jurisdictions covering parks, forests, BLM lands, and water-resource sites. These weren't discretionary grants—they functioned as entitlements tied to acreage and population. The campaign reframed federal land ownership as a fiscal obligation requiring consistent, formula-driven compensation. Alongside fiscal concerns, policymakers also acknowledged that national parks biodiversity preservation served as a compelling justification for maintaining robust federal land management despite the revenue burdens placed on local communities.

How Federal Land Ownership Eliminated Local Property Tax Revenue

The campaign for formula-driven compensation made sense only because federal land ownership had already carved a real hole in local budgets. When Washington acquired private land, it triggered immediate revenue displacement, stripping counties of taxable property overnight. These loss transfers hit hard and fast.

Picture your county facing:

- A shuttered tax roll where a national park now sits

- Roads deteriorating because school and road funds evaporated

- Emergency services stretched thin across federally owned terrain

- Budgets frozen while neighboring counties with private land grew

You couldn't tax federal acres. You couldn't recover that base. The land produced national benefits while your local treasury absorbed the damage alone. That structural imbalance, repeated across hundreds of western counties, built the undeniable fiscal case for legislated compensation. Similar dynamics play out wherever a single governing authority controls vast territory, much like how federal parliamentary constitutional monarchy systems must balance centralized land interests against the fiscal needs of local jurisdictions.

How PILT Payments Were Calculated and Capped

Once lawmakers acknowledged that federal land ownership gutted local tax bases, they'd to design a payment formula that was fair, calculable, and fiscally bounded. The payment formulas they developed tied compensation directly to acreage, setting a cap at $0.10 per acre or $0.05 per acre minus other federal impact aid, whichever was greater. These acreage limits prevented payments from ballooning unpredictably while still guaranteeing a baseline.

Additionally, a population-based ceiling capped total payments relative to local population size. For lands recently acquired into the National Park System or National Wilderness Preservation System, you'd see a separate calculation: one percent of fair market value annually, but only if those lands carried property taxes within five years before acquisition. Governments could spend these payments on any legitimate governmental purpose. Similar efforts to protect purchasing power through fiscally bounded mechanisms were also evident in the Afghan government's currency stabilization measures announced in November 1973, which sought to address inflation while conserving declining foreign reserves.

Which Federal Lands Qualified for PILT Compensation

Eligibility under the 1976 PILT framework wasn't limited to a single agency or land type—it stretched across five distinct federal land categories. If your county contained any of these holdings, you qualified for compensation:

- National Park System lands, including National Monuments your community bordered but couldn't tax

- National Forest System and BLM lands, sprawling across western counties and erasing large chunks of local tax bases

- Water resource development lands, covering reservoirs and flood-control projects reshaping local economies

- Corps of Engineers dredge disposal areas, occupying county land without generating revenue

Notably, Military Bases fell outside this specific entitlement structure. The framework deliberately unified previously fragmented federal payment practices, giving your local government a predictable, formula-driven compensation channel rather than competing for discretionary grants.

What the $117 Million Annual Cost Revealed About the Policy's Scale

Knowing which lands qualified was only half the picture—understanding what the policy would actually cost reveals how seriously Congress took this commitment. When OMB put the annual price tag at roughly $117 million, that number carried real fiscal signaling: the federal government wasn't offering token relief to struggling counties. It was acknowledging a structural obligation at national magnitude.

You can see why that figure mattered. It told local governments they'd receive predictable, formula-driven support rather than discretionary crumbs. It also told skeptics that lawmakers had done the math and still moved forward. Paired with related estimates of $115–$120 million in general-revenue expenditures, the cost picture confirmed this wasn't a marginal experiment—it was a deliberate, large-scale shift in how Washington compensated communities bearing the fiscal weight of federal land ownership.

Why 1976 Became the Foundation of Modern PILT Law

The groundwork laid in 1976 didn't just address an immediate fiscal problem—it restructured the entire relationship between federal land management and local government finance.

Through historical advocacy and persistent legislative precedent, 1976 established the framework that modern PILT law still follows today.

Picture what that framework created:

- Entitlement-based payments replacing unpredictable discretionary grants

- Multi-agency coverage unifying parks, forests, BLM, and water resource lands under one structure

- Population-tied ceilings ensuring proportional distribution across affected jurisdictions

- Acquisition-triggered compensation protecting counties when federal land purchases removed taxable property

You can trace every subsequent PILT reauthorization directly back to these 1976 decisions.

The formula-driven approach transformed local fiscal relief from a political favor into a structured, repeatable federal obligation.