Goods and Services Tax (GST) Introduced

January 1, 1991 Goods and Services Tax (GST) Introduced

On January 1, 1991, Canada replaced its hidden Federal Sales Tax with the visible 7% Goods and Services Tax. Unlike the old embedded manufacturer's tax, you could now see the GST as a separate line on every receipt. Businesses could claim input tax credits, and exported goods left Canada tax-free. The change sparked immediate public backlash and reshaped federal politics for decades. There's much more to uncover about how this tax transformed Canada's entire fiscal landscape.

Key Takeaways

- Canada's Goods and Services Tax launched on January 1, 1991, at an initial rate of 7% applied broadly to goods and services.

- The GST replaced a hidden Federal Sales Tax previously embedded in the prices of manufactured goods.

- Unlike its predecessor, the GST appeared as a distinct, visible line on consumer receipts at the point of sale.

- Businesses could claim input tax credits to recover taxes paid on purchases, with only the final consumer absorbing the full cost.

- The reform triggered widespread public backlash, contributing directly to the Progressive Conservative government's collapse in the 1993 federal election.

What Was the GST and Why Did Canada Need It?

When Canada rang in the new year on January 1, 1991, it also welcomed one of the most controversial tax reforms in its history — the Goods and Services Tax (GST).

Before the GST, Canada relied on a hidden Federal Sales Tax applied only to manufactured goods. You never saw it on your receipt, but you paid it embedded in the product's price. The federal government replaced it with a visible 7% consumption tax to improve tax transparency and consumer fairness.

Instead of taxing goods at the manufacturing stage, the GST applied broadly to goods and services across multiple production and distribution stages. The reform made taxation visible at the point of sale, giving you a clearer picture of what you actually paid to the government.

The Hidden Tax the GST Was Designed to Replace

Before the GST arrived, Canada's tax system quietly extracted money from you through what was called the Federal Sales Tax — a hidden levy baked directly into the price of manufactured goods. You never saw it on a receipt because manufacturers paid it before products ever reached store shelves, embedding those costs invisibly into final prices.

These embedded levies created serious distortions. Businesses couldn't recover taxes paid on inputs, and exporters carried those costs into foreign markets, making Canadian goods less competitive internationally. There were no meaningful production rebates to offset what manufacturers had already surrendered to the federal government.

The GST changed that structure entirely. It made the tax visible, allowed businesses to recover input costs, and shifted the burden to final consumption rather than manufacturing. Similar to how wartime medicine advancements rapidly transformed military healthcare infrastructure by introducing specialized treatment units and improving outcomes, the GST represented a sweeping structural reform designed to replace a broken system with one built for transparency and efficiency.

Brian Mulroney's Drive to Reform the Federal Tax System

That structural overhaul didn't happen by accident — it took a government willing to absorb serious political punishment to push it through. Brian Mulroney and his Progressive Conservative government made federal tax reform a central priority, treating the old Manufacturer's Sales Tax as both economically inefficient and fundamentally dishonest.

The Mulroney reforms weren't popular. Cabinet dynamics shaped the final design, with ministers steering fierce internal debate over rate-setting, exemptions, and provincial relationships. You'd find few politicians keen to attach their name to a new visible tax, yet the government pressed forward anyway.

Mulroney believed replacing a hidden tax with a transparent consumption-based system would strengthen Canada's export competitiveness and modernize federal revenue collection — even if voters punished him for it. Economists and policymakers evaluating the GST's long-term impact can measure its fiscal efficiency by calculating the return on investment of tax reform initiatives against the revenue outcomes they ultimately produced.

The GST at 7%: What It Taxed and How It Worked

Once the GST launched at 7%, it applied broadly to goods and services sold in Canada — a deliberate departure from the old Manufacturer's Sales Tax, which had only hit goods at the production stage. You'd now see the tax clearly listed on tax invoices rather than buried inside product prices.

Businesses collected the GST at each stage of production and distribution, then claimed input credits to recover the tax they'd already paid on business purchases. This prevented tax from piling up at every stage. Only the final consumer absorbed the full cost.

The system made taxation more transparent and treated exports more fairly, since exported goods left Canada free of the federal tax burden. For businesses managing GST filing obligations, compliance deadlines can be calculated precisely by counting the required number of business days from a transaction or reporting period end date.

Why Canadians Suddenly Saw Tax on Every Receipt

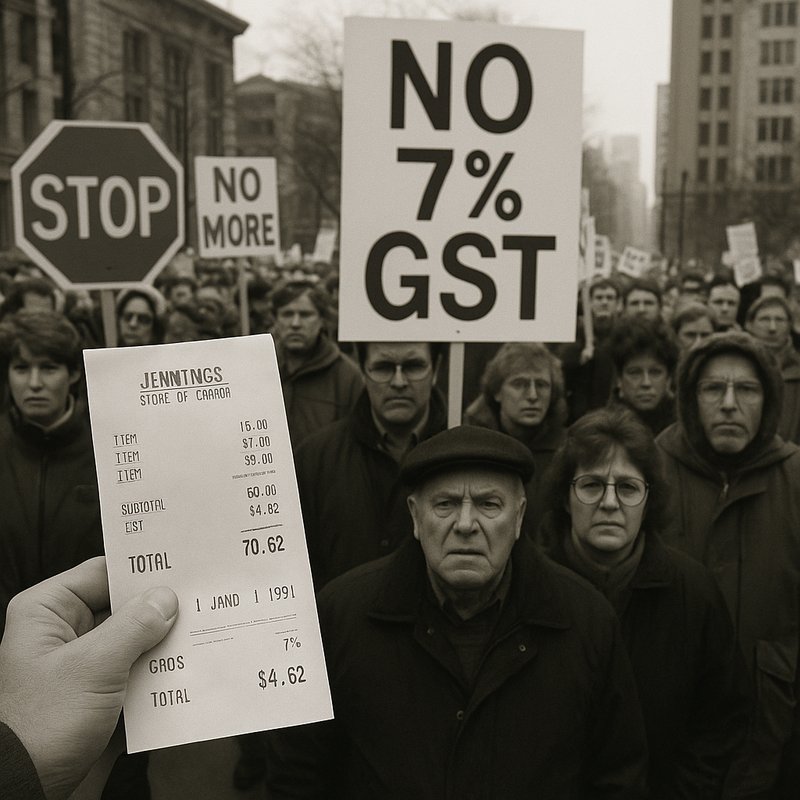

With the GST's launch on January 1, 1991, Canadians encountered something they'd never seen before: a tax line printed directly on their receipts.

Before this, the federal tax was buried inside product prices at the manufacturing stage, so you never saw it. The shift to receipt transparency changed that completely. Every purchase now showed exactly how much federal tax you were paying.

This visibility created immediate consumer awareness. You could suddenly see the 7% GST applied to groceries, services, and everyday goods in real time. While this transparency served the government's reform goals, it also made the tax feel heavier than the old hidden system, even though the overall tax burden had actually shifted rather than simply increased.

The Confusion and Chaos of January 1, 1991

Despite the government's transparency goals, the day after the GST launched was marked by widespread confusion. You'd have walked into stores where cashiers weren't sure how to calculate the new tax, and receipts looked nothing like what Canadians had seen before. Retailers scrambled to update their systems, and many consumers didn't understand what they were suddenly paying for.

The backlash was immediate. Consumer protests erupted across the country, with Canadians openly questioning why everyday purchases now carried a visible 7% charge. Some businesses responded with temporary store closures rather than face the uncertainty of incorrect billing or public anger. The chaos of that first day reflected how dramatically the GST disrupted familiar purchasing habits and materially damaged public trust in the Mulroney government's fiscal agenda.

The Political Fallout That Followed the GST's Launch

The political fallout from the GST's launch hit the Mulroney government hard and fast. You could see the opposition realignment taking shape almost immediately as Canadians directed their anger toward the Progressive Conservatives. The polling collapse was dramatic, erasing what remained of the government's public support.

The backlash reshaped federal politics in three key ways:

- Voter anger drove Canadians away from the PCs in record numbers

- Opposition parties unified their messaging around scrapping the tax entirely

- Public trust in the Mulroney government eroded beyond recovery

The GST didn't just spark short-term frustration. It became a defining political wound that contributed directly to the Conservatives' historic collapse in the 1993 federal election.

GST Rate Cuts: How 7% Became 5% Over Two Decades

Although the GST launched at 7% in 1991, it didn't stay there. By July 2006, the federal government cut the rate to 6%, then dropped it again to 5% in January 2008. You can trace both reductions to the Conservative government under Stephen Harper, who made GST cuts a central campaign promise.

These changes directly shifted tax incidence away from consumers, reducing what you paid on everyday purchases. Critics, however, argued that cutting the GST complicated revenue forecasting, making it harder for Ottawa to project stable federal income over the long term.

Despite the debate, the 5% rate held firm and remained in effect as of 2024. The GST's core structure — taxing consumption visibly — stayed intact even as the rate itself shrank considerably.

How Provinces Responded to the GST and Created the HST

Here's how provinces navigated their options:

- Harmonized provinces merged their sales taxes with the GST, creating the HST and simplifying collection

- Quebec negotiated a unique federal agreement in 1990, administering both its own tax and the GST independently

- Non-harmonized provinces maintained entirely separate systems, leaving consumers managing two visible taxes at checkout

You can still see these differences today.

Provinces that harmonized reduced administrative overlap, while holdouts preserved local control.

The HST ultimately became the clearest outcome of provinces choosing collaboration over independence in responding to federal tax reform.

The GST's Lasting Impact on Canadian Tax Policy

When Canada introduced the GST in 1991, it didn't just change how taxes were collected — it permanently reshaped federal tax policy. You can trace modern consumption tax design directly back to this reform. By replacing a hidden manufacturer's tax with a visible, multi-stage system, the government fundamentally shifted how Canadians understood taxation and influenced consumer behavior at every point of sale.

The GST also redefined fiscal federalism, forcing provinces to reconsider their own tax structures and negotiate new administrative arrangements with Ottawa. Some harmonized their systems into the HST; others maintained separate frameworks. Rate reductions in 2006 and 2008 further demonstrated how politically powerful the tax remained. Today, the GST's core structure continues shaping federal revenue strategy and intergovernmental tax relationships across Canada.