China announces economic growth targets for the year

March 6, 2015 - China Announces Economic Growth Targets for the Year

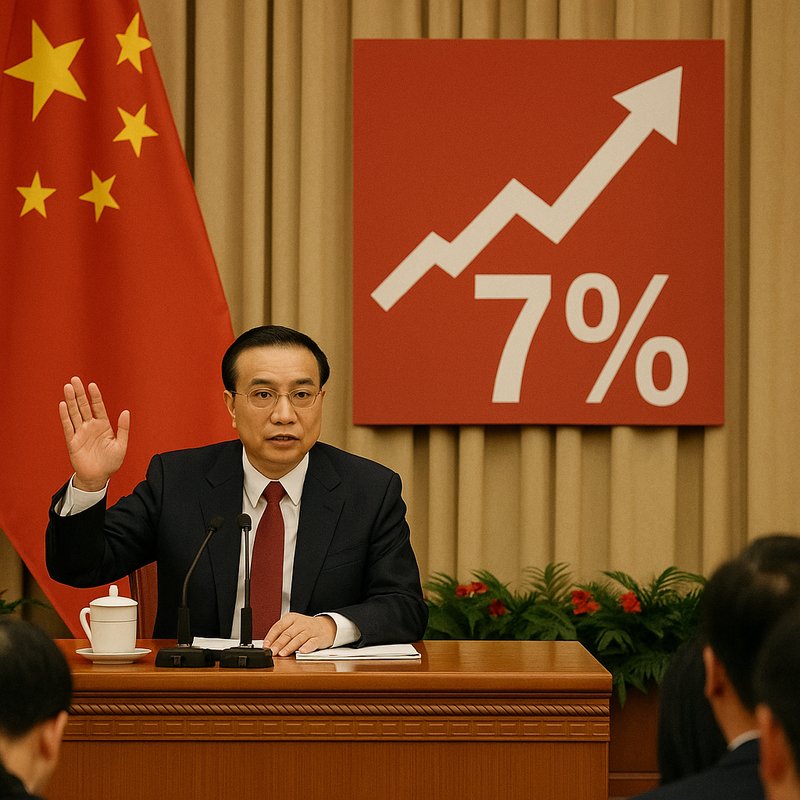

On March 6, 2015, China announced its official GDP growth target of "about 7%" for the year, stepping down from 2014's 7.5% goal. You'll notice this wasn't just a number adjustment — it signaled a deliberate shift toward sustainable, quality-driven growth under what officials called the "new normal." The government also set a 3% inflation target, a 4.5% unemployment ceiling, and pledged to create 10 million jobs. There's much more to this story than the headline figure suggests.

Key Takeaways

- China set its 2015 GDP growth target at "about 7%," stepping down from the prior year's 7.5% goal.

- The inflation target was lowered to 3%, down from 3.5% the previous year.

- China committed to creating 10 million urban jobs while keeping unemployment at or below 4.5%.

- Broad money supply (M2) growth was projected at approximately 12% for 2015.

- The slower growth target reflected a deliberate shift toward sustainable, quality-driven development over maximum output.

China's 7% GDP Growth Target for 2015 Explained

At the annual National People's Congress sessions in March 2015, China announced a 7% GDP growth target — a deliberate step down from the previous year's 7.5% goal. You should understand this wasn't a sign of weakness. It reflected Beijing's acceptance of slower expansion in favor of deeper structural reforms, including currency adjustment and shifting urbanization dynamics.

Officials framed the target as "7% or thereabout," building in flexibility. Beijing had already privately communicated this figure to policy advisors before the formal announcement. The shift signaled a broader strategic pivot — moving away from maximum output toward sustainable economic transformation. China's leadership prioritized quality over speed, aligning near-term growth expectations with the country's long-term reform agenda rather than chasing an artificially inflated headline number. Notably, services grew 8.1% in 2014 and rose to 48.2% of GDP, reinforcing the case that a slower headline growth rate could still support strong employment and household consumption.

The 7% target was also directly tied to a longer-term political commitment: arithmetic projections showed that doubling 2010 GDP by 2020 required average annual growth of at least 6.5% after 2015, making the 2015 target a necessary link in that chain. This period of Chinese economic recalibration unfolded just decades after global conflicts like World War II reshaped international trade relationships, with the formal surrender ceremony aboard the USS Missouri in 1945 marking the beginning of a new postwar economic order that would eventually include China's rise as a global power.

Why China Deliberately Slowed From 7.5% to 7

China's deliberate downshift from 7.5% to 7% wasn't arbitrary — it reflected a structural reality that had been building since 2008. You can see it clearly in the data: productivity growth collapsed from 4.5% annually before 2007 to just 1% afterward, forcing the economy to lean heavily on capital investment instead.

The lower target served as policy signaling — Beijing was acknowledging that debt-fueled expansion had limits. The credit cycle had stretched dangerously, with bank loans flowing to state-owned enterprises rather than productive private firms, misallocating capital across the economy.

Household savings exceeded 30% by 2014, yet financial repression kept those resources trapped in inefficient channels. Slowing the official target wasn't retreat — it was Beijing admitting the old growth engine had fundamentally broken down. Research suggests that if capital allocation efficiency reached U.S. levels, total factor productivity could increase by as much as 30–50%.

The broader economic picture, however, remained uneven across China's geography — 48 largest metropolitan areas, housing just 28 percent of the population, were generating 56 percent of national GDP, revealing how concentrated the country's productive output had become. Canada similarly grappled with concentrated fiscal pressure during this era, passing COVID Special Warrants legislation in 2020 to enable emergency spending when parliamentary oversight was temporarily suspended.

The "New Normal" Strategy Driving China's 2015 GDP Targets

When President Xi Jinping began using the term "new normal" in early 2014, he was signaling something fundamental: China's era of double-digit growth was over, and that was intentional. You're looking at a deliberate pivot from breakneck expansion toward sustainable, quality-driven growth tied to urbanization patterns and environmental sustainability.

The strategy reframes 7% not as a failure to reach higher, but as the middle of an acceptable range — a responsible target aligned with building a moderately prosperous society by 2020. One Peking University professor even benchmarks medium-high growth at 7% for the next two decades.

GDP is no longer the primary scorecard. Reform progress matters more, and China's leadership is betting that slower, structured growth builds a stronger long-term foundation. In 2014, China's service sector value added rose to 48.2% of GDP, reflecting the structural shift away from industry-led expansion that underpins this longer-term vision. This kind of structural realignment mirrors broader governance trends seen globally, such as Canada's 1995 move to establish a statutory departmental authority for industry-related programs through formal legislation.

The target was formally announced in Premier Li Keqiang's government work report at the National People's Congress, underscoring that the new growth framework carries the full weight of state institutional authority.

How Household and Government Spending Were Built Into the 7% Target

Consumption forms the backbone of China's 7% growth math. Together, household and government spending add RMB 3.5 trillion, covering 3.9 GDP points in 2015. Transfer reform strengthens government's role by redirecting funds toward education and healthcare rather than industry subsidies. Household resilience keeps consumer spending growing 8–12% annually, making it the most predictable growth driver. China's high domestic savings rate, historically around 32% of GDP, provided the capital foundation that made sustained consumption and investment growth possible. Brazil's 1998 amendment to its Agricultural Policy Law similarly demonstrated how unified sanitary oversight can reshape economic frameworks by consolidating inspection and risk-control systems under a single institutional structure.

Here's how the numbers break down:

- Household spending adds RMB 2.5 trillion at 10.7% nominal growth

- Government spending contributes RMB 960 billion from a RMB 9 trillion base

- Combined, both sources generate roughly $1 trillion in new activity

- Together, they push China's output past the $10.4 trillion 2014 baseline

If consumption disappoints, investment must fill the gap, risking debt and reform credibility.

China's 2015 Inflation and Jobs Targets, Explained

While growth commanded the headlines, inflation and jobs targets quietly shaped the 2015 policy framework just as decisively. China set its official inflation target at 3 percent, down from 3.5 percent the prior year. By May, you'd see actual inflation dynamics running well below that ceiling at just 1.2 percent, raising deflation concerns despite four PBOC rate cuts in six months.

The PBOC pushed benchmark lending rates to 4.85 percent and trimmed reserve requirements to stimulate borrowing and lift prices. On the employment threshold, China's NAIRU held steady at 4.0–4.1 percent since 2000, directly tying the 7 percent growth target to job preservation. You can't understand the 2015 framework without recognizing how closely inflation control and employment stability were intertwined. The government paired these targets with a commitment to create 10 million jobs while keeping the urban unemployment rate at or below 4.5 percent for the year.

Complementing these targets, the government projected broad money supply growth at about 12 percent, signaling a monetary stance calibrated to support both price stability and continued economic expansion without overstimulating an already-slowing economy.

What Xi and Li Actually Pledged at the 2015 Work Conference

At the 2015 Work Conference, Xi Jinping and Li Keqiang committed China to a sweeping agenda that tied slower growth explicitly to structural transformation. Their party priorities centered on supply-side reforms, rural revitalization, and quality-driven development. Here's what they actually pledged:

- Supply-side reforms — fewer housing curbs, targeted tax cuts, and industry-specific incentives

- SOE restructuring — executive salary cuts and deeper state enterprise overhauls

- Social commitments — expanded medical reforms, poverty alleviation, and rising personal incomes

- Financial liberalization — regulatory reforms alongside deeper financial sector changes

You'll notice these pledges weren't abstract—they addressed real structural bottlenecks. Xi and Li essentially reframed slower GDP growth not as failure, but as the deliberate price of building a more sustainable, efficient economy. A key part of this strategy involved targeting 274 million migrant workers as potential buyers to help absorb the country's massive inventory of unsold homes. Expanding China's economic reach beyond its borders was also a stated priority, with the conference pledging to encourage Chinese companies to invest overseas and promote the yuan internationally as part of a broader marketization agenda. Underpinning these ambitions was China's rapidly evolving digital infrastructure, where mobile search penetration had already exceeded 99%, reshaping how both consumers and businesses accessed economic information and opportunities across the country.

Can China Miss Its Own GDP Growth Target Without Consequence?

When China reported 7.4% growth for 2014—missing its 7.5% target by just 0.1 percentage points—it raised an uncomfortable question: does missing the target actually matter?

The short answer is: not much, practically speaking. The symbolic hit was real, but there wasn't serious political fallout. Beijing had already rebased 2013 GDP upward by 3.4% following an economic census, which complicated direct comparisons and raised questions about statistical credibility.

What mattered more was the narrative. China's services sector hit 48.2% of total GDP, signaling a genuine structural shift.

Heading into 2015, Beijing whispered a "7% or thereabout" target—language that built in flexibility. Missing by 0.1% again wouldn't derail reforms. It'd simply reinforce that growth quality now outranks growth speed. Online retail sales surged 33.3 percent year-on-year, demonstrating that consumption patterns were rapidly evolving alongside the broader structural transformation. This kind of symbolic yet substantive framing echoed how other governments use declaratory motions—much like when Canada's House of Commons passed a motion 265 votes to 16 recognizing the Québécois as a nation within a united Canada, signaling identity without triggering binding legal change. By year's end, tertiary industry would account for 50.5% of GDP, further cementing that the economy's center of gravity had durably shifted away from manufacturing and toward services.

How the 2015 Target Fits China's 2020 GDP Doubling Goal

China's 2015 target of "7% or around 7%" wasn't arbitrary—it's the pace Beijing needs to fulfill its 2020 pledge of doubling 2010 GDP. Earlier strong growth created a buffer, but you still need consistent execution.

Here's what makes 7% the critical number:

- Baseline math: Doubling 2010 GDP requires ~7.2% average annual growth through 2020

- Buffer advantage: 2011–2014 averaged above 9%, giving China room to slow

- Infrastructure upgrades: Sustained investment keeps capital formation contributing 3.2 growth points

- Demographic transition: Expanding services absorbs workforce shifts as manufacturing cools

Miss this pace consistently, and the doubling goal slips. Hit it, and Beijing validates its "new normal" as deliberate, not distressed. Similar precedents exist elsewhere, as Brazil's Manaus Free Trade Zone demonstrated how targeted incentive mechanisms can reshape regional economies and attract both domestic and foreign investment over the long term. Reinforcing this confidence, the service sector has already surpassed manufacturing in size, signaling that China's structural shift is underway rather than merely promised.

Why the 7% Target Signaled a Permanent Shift in China's Growth Model

Beyond the math of doubling GDP, the 7% target carried a deeper message: Beijing wasn't just slowing down—it was deliberately changing direction. You could see it in the language Premier Li Keqiang used—"high-quality development," "supply-side structural reform," and innovation-led urbanisation replaced the old obsession with raw output.

This structural transition meant China was stepping away from debt-fueled stimulus and industrial overcapacity toward a productivity focus built on services, consumption, and efficiency. The days of double-digit growth powered by investment binges were officially over. Decades later, Premier Li Qiang would present a government work report at the National People's Congress setting a 4.5 to 5 percent growth target for 2026, underscoring how profoundly China's growth ambitions had been recalibrated over time.

That 2026 target also marked only the third time China had adopted a growth range, with prior instances in 2016 and 2019, reflecting an institutional acknowledgement that economic uncertainty had become too significant to manage with a single fixed number. Much like the geopolitical shockwaves triggered by the Soviet space programme—which prompted the United States to establish NASA in 1958 and dramatically restructure its scientific and defence priorities—China's growth recalibration similarly reshaped global economic expectations and forced competing nations to reassess their own development strategies.