China announces new infrastructure investment plans

August 29, 2018 - China Announces New Infrastructure Investment Plans

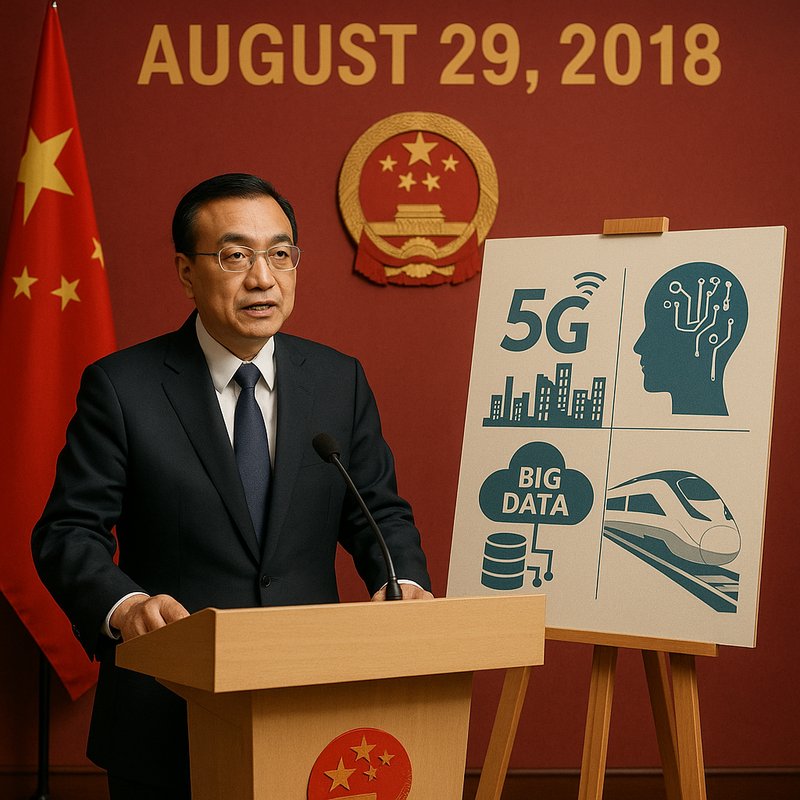

On August 29, 2018, China's government announced a major pivot away from traditional large-scale developments toward high-tech, digitally driven investment. You're looking at a strategic shift prioritizing 5G, artificial intelligence, big data, and high-speed rail to fuel economic growth and create high-value jobs. It's a framework tightly aligned with five-year planning priorities and the ambitious Made in China 2025 agenda. If you want the full picture, there's a lot more to uncover here.

Key Takeaways

- China announced a strategic shift from conventional large-scale developments toward green growth, digital connectivity, and high-tech infrastructure investment.

- Priority technologies included 5G, artificial intelligence, and big data, designed to generate high-value employment and retain skilled talent.

- The 2018 funding mix comprised 58% self-funding, 18% domestic loans, and 17% national budget allocations.

- Investment aligned with five-year planning priorities and integrated with international initiatives, notably the Belt and Road Initiative.

- State-backed financial instruments, including low-interest loans and direct subsidies channeled through state-owned enterprises, funded these infrastructure programs.

What Is China's New Infrastructure Plan?

China's new infrastructure plan is an ambitious central government policy that channels investment into high-tech sectors to kickstart economic growth, boost future jobs, and drive technological innovation. It reimagines traditional infrastructure stimulus for the 2020s, targeting seven key industry sectors unified by their intelligent systems potential.

You'll find the plan goes beyond simple construction projects. It's a strategic framework for economic restructuring, shifting China away from conventional large-scale developments toward green growth and digital connectivity. By prioritizing cutting-edge technologies like 5G, artificial intelligence, and big data, the plan creates high-value employment opportunities that support talent retention across emerging industries.

It also aligns with China's broader five-year planning priorities, integrating with international initiatives like Belt and Road to strengthen global connectivity and long-term competitiveness. The Belt and Road Initiative, launched in 2013, saw roughly $1 trillion in investment and construction deals with partner countries over its first decade. As foreign investments increasingly draw government scrutiny worldwide, countries like Canada have updated their national security review frameworks to better assess the implications of large-scale inbound investment.

What Triggered China's 2018 New Infrastructure Push?

Several factors converged in 2018 to push China's government toward its new infrastructure agenda. You'll find the domestic catalysts rooted in economic stress: GDP growth hit a decades-low 6.6%, steel and cement overcapacity demanded new investment outlets, and local government debt reached 40 trillion yuan. Unemployment risks from industrial slowdowns made job-creating projects essential.

The geopolitical drivers were equally significant. The US-China trade war erupted in March 2018, threatening $100 billion in exports, forcing Beijing to strengthen regional connectivity as a counterbalance. Simultaneously, 147 countries had signed BRI agreements, creating reciprocal infrastructure obligations. The Asian Development Bank identified a $900 billion annual infrastructure gap across Asia, giving China a strategic opening to expand influence while absorbing its domestic industrial overcapacity through foreign and internal infrastructure projects. China also pursued the renminbi internationalization agenda alongside infrastructure expansion, seeking to reduce financial dependence on Western-dominated monetary systems.

In 2016, China established the Asian Infrastructure Investment Bank to fund infrastructure development, providing an institutional financing mechanism that complemented the broader Belt and Road Initiative and attracted membership from major Western economies including the United Kingdom, Germany, and France.

Why Made in China 2025 Can't Happen Without New Infrastructure

Made in China 2025 demands infrastructure that simply doesn't exist yet. Current factories can't support the 70 percent domestic content targets across semiconductors, electric vehicles, robotics, and aerospace. You're looking at labor-intensive workshops that need complete transformation into smart manufacturing hubs—a shift that'll reshape labor relations as automation displaces traditional workforces.

Regional innovation hubs in the Yangtze River Delta and Greater Bay Area require transportation networks, 5G connectivity, and integrated logistics systems that currently aren't in place. Supply chains need redundant distribution pathways to eliminate foreign technology dependency. China's semiconductor ambitions mirror the IP licensing model that allowed ARM-designed chips to reach over 10 billion units shipped worldwide by 2008, underscoring how intellectual property infrastructure can be just as critical as physical infrastructure.

Smart manufacturing also demands cloud computing infrastructure, data centers, and cybersecurity systems. The environmental impact of building hundreds of new R&D centers and redesigned production facilities adds another layer of complexity you can't ignore. China has committed to constructing 40 R&D centers across the country by 2025 to anchor this infrastructure push.

The plan's funding mechanisms rely heavily on state-backed financial instruments, including low-interest loans and direct subsidies, channeled through state-owned enterprises that account for roughly one-third of China's GDP.

The Seven Core Areas of China's New Infrastructure Plan

Beijing's new infrastructure blueprint targets seven core areas that form the backbone of China's digital and physical transformation.

You'll see 5G Expansion driving 600,000–800,000 base stations for prefecture-level coverage, while Big Data centers build tiered computing clusters supporting industrial digitization.

AI Robotics anchors embodied intelligence and manufacturing integration, reinforcing China's competitive edge against the US.

High Speed Rail connects cities through multi-dimensional networks, including 150+ Greater Bay Area projects.

Converged Systems tie electricity grids, smart storage, and space internet into unified operational platforms.

The Low Altitude Economy leverages 5G infrastructure to enable drone sectors and intelligent systems.

Each area interlocks deliberately—5G feeds AI, AI optimizes rail, and converged systems coordinate energy with data, creating infrastructure dependencies that accelerate China's broader technological ambitions. Clean energy sectors now make up 11.4% of GDP, nearly doubling since 2022, underscoring how deeply embedded energy transformation has become within China's broader industrial and infrastructure strategy. This mirrors the kind of interconnected dependency seen in entertainment-driven economies, where Korean entertainment exports are projected to double their Hollywood reach by 2027 through sustained co-production investment. China's 15th Five-Year Plan (2026–2030) further reinforces this trajectory, unveiling a package of major infrastructure initiatives that spans from multi-dimensional transportation to a national integrated computing network.

How Much Is China Spending on New Infrastructure?

Understanding the scale of China's infrastructure ambition requires looking at the numbers behind it.

New infrastructure investment in 2021 reached RMB 1.16 trillion, covering urban renewal, smart mobility, and digital twins technology. While that trails traditional infrastructure spending, it's growing fast.

China's broader overseas engagement tells an even bigger story.

Since 2005, combined overseas investment and construction have exceeded USD 2.5 trillion. BRI construction contracts alone hit USD 775 billion cumulatively since 2013.

Financing these projects relies heavily on domestic mechanisms.

In 2018, 58% came from self-funding, 18% from domestic loans, and 17% from national budgets. Green bonds and private capital are increasingly filling gaps, particularly as private sector players now dominate newer BRI investment rounds across energy, mining, and digital infrastructure. The tracker covering this activity spans 4,900 large transactions across metals, property, agriculture, and other sectors, representing the only comprehensive public dataset of its kind. Meanwhile, the commercial space sector presents a parallel shift toward private-led infrastructure, with the commercial space station market projected to reach nearly $12.93 billion by 2030, reflecting how private capital is reshaping strategic industries globally.

The first half of 2025 marked a significant milestone in BRI activity, with total engagement reaching USD 124 billion across approximately 176 deals in a single six-month period.

Which Regions Moved First on New Infrastructure?

China's infrastructure rollout didn't happen evenly—certain regions moved first, driven by strategic priorities rather than economic readiness.

Tibet upgrades came early and aggressively, with highway systems growing 51% between 2015 and 2020 and high-speed rail connecting Lhasa to Nyingchi by 2021. These moves prioritized military logistics and border reinforcement over civilian demand.

Xinjiang followed a similar pattern, expanding its rail network from 5,900 km to 7,800 km by 2020 while building dual-use airports near sensitive borders.

Meanwhile, the Greater Bayway region accelerated commercial integration, fusing 11 cities into a high-speed, hyper-connected economic zone through coordinated 2017 agreements.

You can see the pattern clearly: border regions got military-driven infrastructure first, while economic hubs like the Greater Bay Area received connectivity investments designed to maximize trade output. Together, Tibet and Xinjiang account for roughly 30% of China's total territory, underscoring why securing and connecting these vast frontier regions became a top national priority. Xinjiang's strategic location was also explicitly recognized within the BRI framework, as the region connects multiple neighboring countries and serves as a critical land bridge for the Silk Road Economic Belt corridors extending into Central Asia and beyond. This kind of state-directed, dual-purpose infrastructure development echoes earlier precedents in other nations, such as Britain's Calder Hall nuclear plant, which was publicly celebrated as a commercial milestone while simultaneously serving a primary military mission of weapons-grade plutonium production.

How Huawei, Alibaba, and Foreign Firms Fit Into the Build-Out

The infrastructure rollout you've seen across Tibet, Xinjiang, and the Greater Bay Area didn't build itself—it ran on technology supplied by a tight circle of national champions and, in some cases, carefully managed foreign partners. Huawei's 5G networks and Alibaba's City Brain AI handle the operational backbone, aggregating citizen data while reinforcing data sovereignty under state oversight.

Both firms align directly with Made in China 2025 and the Digital Silk Road, turning smart city pilots into export templates for BRI nations. Foreign firms do participate, but China controls the terms. Vendor diversification exists only where it serves Chinese strategic goals—foreign telecom partnerships, for instance, accelerate 5G deployment without ceding platform control or data access to outside actors. By April 2019, Chinese firms were participating in 52 standard-setting initiatives across 34 countries, positioning themselves to shape the equipment, services, and technology norms that underpin these deployments globally.

China's digital expansion into the Global South stretches back further than most assume—Huawei first entered the African telecom market in 1998, establishing an early commercial foothold that preceded the formal Digital Silk Road framework by nearly two decades. Samsung, meanwhile, has pursued a parallel infrastructure ambition, positioning its 5G industrial infrastructure as the connective layer between autonomous factories, mobility systems, and AI deployments across global markets.

How China Is Using New Infrastructure to Project Global Power

When you look at what China has built since 2005—nearly fivefold capacity growth while U.S. output stayed flat—it's clear this isn't just a domestic energy story.

China's grid dominance is becoming a tool of soft power, giving it leverage across trade corridors where energy infrastructure precedes political influence.

By exporting UHV technology, AI-driven grid systems like "Guangming Power," and renewable buildout expertise, China's practicing digital diplomacy at scale.

Partner nations that adopt Chinese energy frameworks increasingly align with Chinese standards, supply chains, and financing.

Even cultural exports follow the infrastructure—where China builds, its broader economic ecosystem follows.

With $500 billion invested in 2025 alone, China isn't just modernizing its own grid; it's positioning itself to shape how the world powers its future. China's solar capacity alone reached 1.20 terawatts by end-2025, surpassing the total installed power capacity of many advanced economies combined.

Global energy transition investments exceeded $2 trillion in 2024, with China accounting for nearly 40% of global investment, cementing its role as the dominant force behind the worldwide shift toward clean energy infrastructure. Just as Salesforce's multi-tenant cloud architecture disrupted enterprise software by enabling automatic updates and eliminating costly installations, China's standardized energy infrastructure exports are rewriting the rules of how nations adopt and depend on foreign-built systems.