China expands international trade agreements

April 9, 2014 - China Expands International Trade Agreements

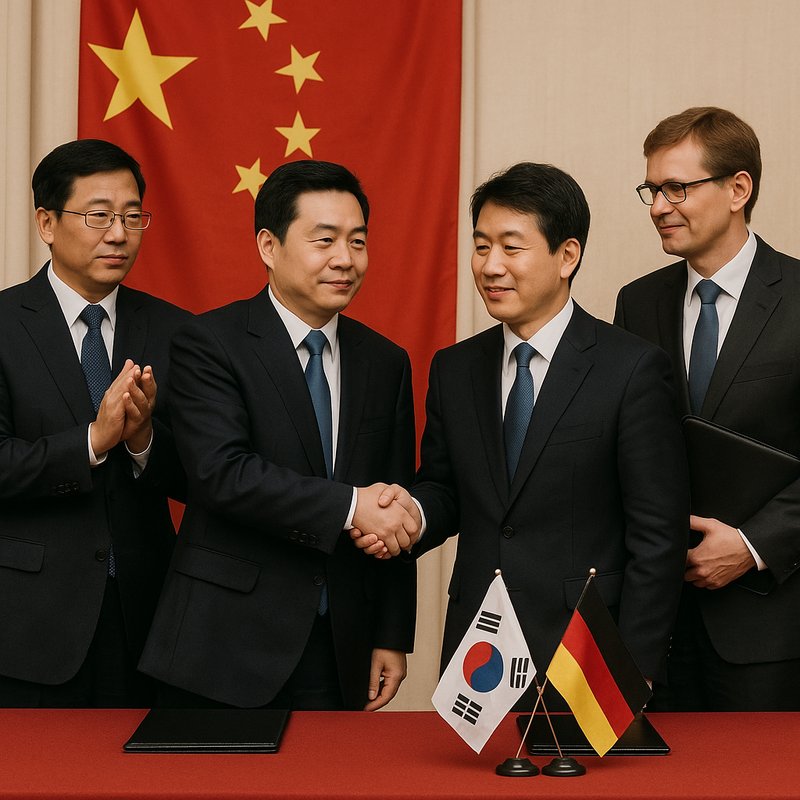

On April 9, 2014, you're looking at a pivotal moment when China joined the ITA expansion and extended RQFII access to South Korea and Germany. The ITA move eliminated tariffs across 201 ICT product categories, unlocking roughly $12 billion in export gains concentrated in semiconductors and electronics. The RQFII extension built new offshore RMB hubs, attracting long-term foreign capital into Chinese markets. These weren't isolated moves — they were part of a much larger strategy you'll want to explore further.

Key Takeaways

- On April 9, 2014, China joined the ITA expansion, committing to eliminate tariffs across 201 ICT product categories.

- Average tariff rates on select ICT items dropped from 5–10% to zero following China's ITA commitment.

- China's ITA participation generated approximately $12 billion in export gains, concentrated in semiconductors and finished electronics.

- China leveraged assembly specialization in chiplet modular supply chains to maximize competitive advantages from the tariff eliminations.

- The ITA expansion complemented China's broader 2014 trade strategy, which included APEC chairmanship and active bilateral FTA negotiations.

Where China Stood in Global Trade Before 2014

China's trade story begins with humble origins — in 1978, the country ranked 32nd globally, handling just $20.6 billion in import/export volume and claiming less than 1% of world trade. You can trace its export evolution from primary products in the pre-1980s through manufactured goods, then light industrials, and finally into high-tech electronics and IT.

By 2001, WTO accession unlocked lower tariffs and dispute settlement access, accelerating growth to $2.974 trillion by 2010 — 144 times the 1978 level. China's trade resilience showed clearly when it became the world's leading trading nation in 2013, surpassing the United States.

Entering 2014, it held a 10.6% global share, maintained relationships with 231 countries, and projected continued growth well ahead of world trade averages. The mid-1990s emergence of global value chains allowed China to integrate into fragmented international production networks, laying critical groundwork for the export dominance it would achieve in the years that followed.

China has since developed a vast network of economic relations spanning industrial, semi-periphery, and periphery countries, with its largest trading partners shifting over time in response to major policy changes. As foreign investments into partner economies have grown, host nations have increasingly updated frameworks like the Investment Canada Act to strengthen national security oversight of inbound capital flows.

Why China Extended RQFII Access to Korea and Germany?

By April 2014, China had extended its Renminbi Qualified Foreign Institutional Investor (RQFII) program to South Korea and Germany — but why these two countries, and why then?

China was actively building RMB hubs beyond Hong Kong, having already expanded to London and Singapore in 2013. Seoul and Frankfurt were natural next steps, giving Chinese authorities broader offshore channels to raise RMB capital for onshore investments.

Market liberalization was also a driving force. China needed long-term foreign capital flowing into its A-shares and bonds while gradually loosening capital account restrictions. By extending RQFII access, China responded directly to growing global investor demand for China exposure.

You can see the strategy clearly: attract more institutional players, diversify offshore RMB centers, and steadily integrate China's financial markets with the wider world. Unlike QFII, RQFII allows investment using offshore RMB directly, removing the need for foreign currency conversion and making participation more accessible to international institutions. This drive toward interconnected financial infrastructure echoed broader trends in global standardization, much as GSM standardization slashed manufacturing costs and eliminated fragmentation to make 2G the dominant worldwide communications infrastructure.

Regulators had also signaled that quotas could be removed entirely once market conditions and capital account liberalisation were sufficiently advanced, underscoring that the RQFII expansions into Korea and Germany were part of a longer-term structural shift rather than isolated policy decisions.

How the ITA Expansion Boosted Chinese ICT Exports by $12 Billion?

While China was reshaping its financial architecture through programs like RQFII, it was simultaneously pushing into another front: trade liberalization for high-tech goods. On April 9, 2014, China joined the ITA expansion, committing to eliminate tariffs across 201 ICT product categories.

The tariff passthrough was immediate on select items, dropping average rates from 5–10% to zero and unlocking roughly $12 billion in export gains. You'll notice those gains concentrated heavily in semiconductors and finished electronics. The semiconductor supply chain underpinning those exports relied heavily on chiplet modular design, where functions like compute, memory, and I/O are fabricated independently and linked via inter-die protocols to improve yields and lower production costs.

China's edge wasn't deep innovation — it was assembly specialization, converting imported components into exportable products with maximum efficiency. US imports from China climbed 6% to $466.7 billion, with ICT-heavy sectors driving much of that expansion. The ITA didn't transform China's tech depth; it amplified what China already did best. That amplification showed up clearly in China's full-year trade data, where the overall trade surplus reached $382.46 billion, a record high representing a 47.2% increase over 2013.

Latin America emerged as a significant beneficiary of China's expanding export machine, with electrical machinery exports alone reaching USD 58 billion in 2024 as the region absorbed growing volumes of Chinese ICT and industrial goods. Exports to the region nearly doubled over the decade, reflecting the durable demand unlocked in part by trade liberalization efforts like the ITA expansion.

How South China Sea Access Shaped China's Regional Trade Routes?

The South China Sea isn't just a body of water — it's the backbone of China's regional trade architecture. When you examine the numbers, the strategic weight becomes undeniable. Five trillion dollars in annual trade flows through these sea lanes, representing:

- Half of global daily merchant shipping

- One-third of global oil trade

- Two-thirds of global LNG trade

- Oil volumes tripling the Suez Canal's capacity

China's resource security depends heavily on maintaining uninterrupted access through these corridors. Military modernization directly supports SLOC protection from the Gulf of Arabia to China's eastern seaboard. Disruptions aren't hypothetical — a blockage scenario forces rerouting south of Australia, triggering welfare losses across nearly every trading nation. Taiwan alone faces a 34% real income loss, confirming how deeply interconnected these routes remain. To reduce exposure to such vulnerabilities, China developed CPEC as a land-based alternative routing oil supplies through Gwadar, directly addressing its Malacca Strait dependence. The sea also holds extraordinary resource potential, with CNOOC estimating approximately 125 billion barrels of oil and 500 trillion cubic feet of gas in undiscovered areas alone, further reinforcing China's strategic imperative to maintain dominance over the region.

Why China Wanted to Lead Trade Across the Asia-Pacific?

When the United States withdrew from the Trans-Pacific Partnership in 2017, China saw an opening it couldn't ignore. By applying to join the CPTPP in September 2021, China pursued regional leadership across the Asia-Pacific, positioning itself as a champion of free trade while the US stepped back.

This wasn't just symbolic. China used economic statecraft to offset Trump-era tariffs, gain access to markets in Japan, Australia, and Canada, and counter Western decoupling efforts. Joining a high-standard pact with 11 members meant expanded influence and a direct challenge to US allies.

China also blocked Taiwan's simultaneous application, reinforcing its territorial claims. Every move served a dual purpose: boost trade at home while reshaping the Asia-Pacific's economic order on China's terms. Notably, China's application was submitted one day after Aukus was announced, revealing the strategic precision behind its timing.

Despite these ambitions, China's economic footprint in Southeast Asia tells a more complicated story. While China is the largest bilateral trading partner in goods for all ASEAN states, the region runs a chronic trade deficit with China, and Chinese FDI into the region persistently lags behind investment from the EU, the United States, and Japan. Reinforcing its domestic economic position, China has invested over 100 billion yuan in AI development over the past three years, signaling that technological self-sufficiency is as central to its global strategy as trade expansion.

Shanghai FTZ Reforms That Unlocked Foreign Investment Channels

China's push for regional dominance through trade pacts like the CPTPP tells only half the story—the other half plays out on home turf, inside the Shanghai Free Trade Zone (SFTZ).

Through RMB liberalization and reinvestment incentives, the SFTZ hands you concrete tools to move capital efficiently:

- Convert foreign currency for outbound direct investment through SFTZ banks

- Borrow RMB from overseas lenders without pre-approval for direct overseas investment

- Reinvest undistributed profits via new enterprises, capital increases, or share acquisitions

- Access fast-track processes through the expanded QFLP pilot for domestic equity investment

These reforms don't just open doors—they remove the bureaucratic friction that once made foreign capital hesitate before entering China's financial ecosystem. Much like how Claude Shannon's 1937 thesis demonstrated that connecting the right structural framework to an existing system could unlock transformative practical applications, the SFTZ's regulatory architecture transforms theoretical capital mobility into operational reality. Eligible foreign investors are also encouraged to establish investment companies and regional headquarters in Shanghai, where they receive foreign-funded enterprise treatment in accordance with national regulations. Foreign-invested enterprises seeking to expand can further benefit from support to apply for ultra-long-term special treasury bonds to fund large-scale equipment renewal and technological upgrade projects in key areas.

How RCEP and FTAAP Pulled ASEAN Economies Toward Beijing?

Signed in 2020, RCEP didn't just expand regional trade—it quietly pulled ASEAN economies into Beijing's gravitational orbit. China's enthusiasm for the deal deepened ASEAN-Beijing economic ties, even amid bilateral tensions. The agreement consolidated existing ASEAN+1 FTAs, covering 90% of intraregional trade, while delivering the largest tariff cuts to China, Japan, and South Korea. That asymmetry matters. You'll notice ASEAN's balance of trade actually deteriorated 6% annually post-RCEP, with imports outpacing exports across most member states.

Beijing's political influence grew alongside supply chains increasingly anchored to Chinese production networks. While harmonized rules of origin theoretically shift some manufacturing to lower-cost ASEAN countries, the structural pull remains toward China. ASEAN gains less here than from CPTPP—yet it's RCEP shaping the region's economic trajectory. Analysts project RCEP will raise the trading bloc's GDP by approximately 0.4% by 2030, reflecting modest but measurable economic integration gains concentrated among its members.

The depth of regional integration becomes clearer when examining intra-RCEP trade flows, which saw member countries accounting for 50% of total imports by 2018, underscoring how thoroughly these economies had already woven themselves together before the agreement was even signed. Negotiations for RCEP began in 2012 and spanned more than eight years before culminating in the landmark deal. Much like Canada's transcontinental railway promise, which bound British Columbia to Confederation by guaranteeing national defense routes that avoided U.S. territory, RCEP's architecture similarly reflects how infrastructure and trade frameworks are engineered to consolidate sovereignty and reduce dependence on rival powers.

China's Free Trade Deals With Switzerland, Iceland, and Hong Kong

Three free trade agreements—with Iceland, Switzerland, and Hong Kong—reveal how China systematically built its European and regional trade architecture one strategic partnership at a time.

Each deal carried distinct strategic weight:

- Iceland (2013): Zero tariffs on 99% of Chinese industrial exports, opening Arctic access, fisheries management ties, and tourism cooperation

- Switzerland (2013): Covered IP, competition, labor, and Chinese medicine cooperation

- Hong Kong (CEPA, 2003–2024): Deepened services trade integration with 2024 supplement updates effective March 2025

- EFTA positioning: China's EFTA agreement (2011) set the regional foundation both deals built upon

You can see China's pattern clearly—Iceland delivered geographic leverage, Switzerland unlocked continental credibility, and Hong Kong reinforced regional integration.

Together, they position China for broader European and global trade expansion. The Switzerland deal, notably the first FTA signed between China and a continental European country, entered into force on 1 July 2014. China also maintains active free trade agreements with partners across Latin America and Asia-Pacific, including Chile, Pakistan, and Peru, further reflecting the breadth of its global trade network. Underpinning these expansive trade activities is each nation's need to manage borrowing authority legislation that funds government operations and supports the fiscal frameworks enabling international trade commitments.

How China's 2014 Agreements Reached 22 Trade Partners?

By 2014, China had built out a trade network spanning 22 partners—blending APEC-driven multilateral ambitions with targeted bilateral upgrades across Asia-Pacific and Latin America. You can trace this expansion through deliberate trade diplomacy: China chaired APEC in 2014, proposing the FTAAP feasibility study covering over 60% of the world economy, while simultaneously elevating bilateral ties with New Zealand and advancing FTAs with Chile, Peru, and Costa Rica.

Each agreement deepened tariff harmonization across agriculture, financial services, and energy sectors. Australia's FTA talks in 2014 pushed bilateral trade to $107.8 billion. Latin America added nine strategic partnerships, three carrying full FTA status. Together, these moves transformed China's pre-2014 foundation into a comprehensive Pacific Rim trade architecture you can clearly track today. Unlike the TPP and RCEP, APEC's inclusive membership structure offered a distinct advantage because it brought both China and the US into the same trade framework simultaneously. This era of expanding trade networks mirrored earlier technological milestones in global connectivity, such as when Telstar 1 relayed the first live transatlantic television broadcast in July 1962, demonstrating that real-time international communication could reshape economic and diplomatic relationships overnight.

Among China's bilateral agreements active during this period, the CEPA framework with Hong Kong stood out as a foundational model, having entered into force on 29-Jun-2003 and continuing to evolve through successive supplements and liberalisation rounds well into the 2020s.

How These Deals Shifted $640 Billion in Global Capital?

China's 22-partner trade network didn't just redraw maps—it redirected hundreds of billions in global capital. By 2014, trade diversion and investment reallocation reshaped where money moved globally. You're seeing capital shift away from Western manufacturing toward Chinese production hubs, driven by:

- 377 regional trade agreements in force globally

- RCEP projected to add $500 billion to world trade by 2030

- China's trade surplus holding at $216 billion annually

- Investment exceeding 50% of China's GDP

These deals accelerated capital concentration in China's favor. Western firms weren't just trading—they're funding a rival system. China's state-driven model proved itself as a legitimate alternative, pulling investment reallocation decisions away from traditional Western-aligned markets toward Beijing's expanding commercial sphere. The deeper integration of China into global trade following WTO accession had already lifted hundreds of millions out of poverty, demonstrating the transformative power of Beijing's state-directed economic model on the world stage. Between 2003 and 2019, U.S. officials challenged China 23 times in WTO proceedings, underscoring the growing legal and institutional friction embedded within this expanding trade rivalry. As global supply chains deepened, technology conglomerates like Samsung—whose semiconductor and manufacturing operations account for 25% of South Korea's GDP—found their cross-border production strategies increasingly shaped by the shifting terms of this China-centered trade architecture.