China expands international trade partnerships

April 25, 2016 - China Expands International Trade Partnerships

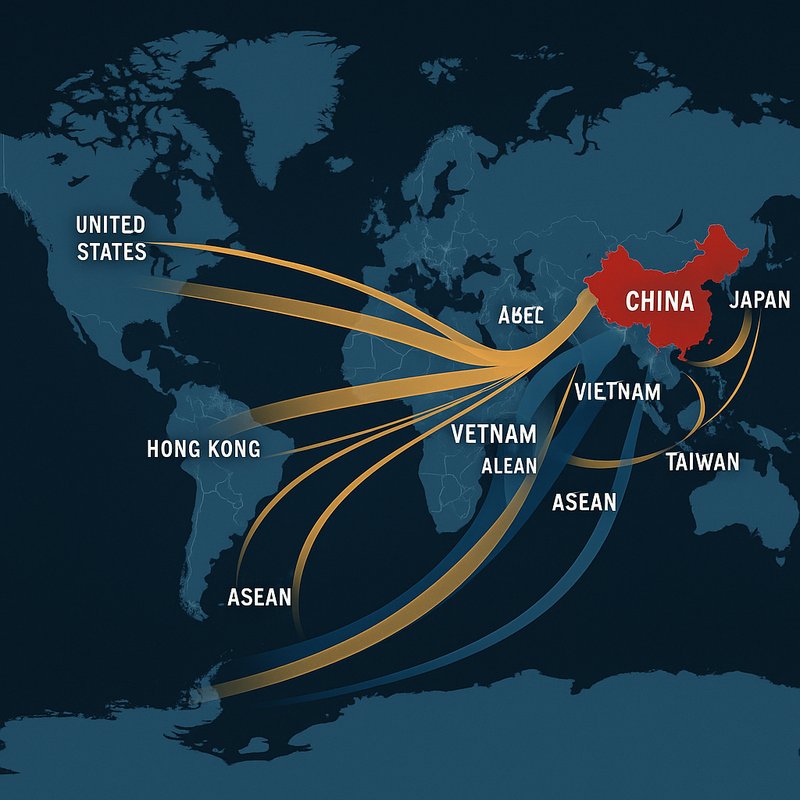

On April 25, 2016, you can trace the moment China's export machine reached its widest global footprint yet — with the U.S., Hong Kong, and Japan anchoring a trade network that stretched from Southeast Asia to the Middle East. South Korea held fourth place, while ASEAN nations and Vietnam emerged as growing destinations. Germany and Taiwan reinforced China's diversified reach. By 2025, China's exports are projected to represent 15.8% of world exports — and there's much more to uncover.

Key Takeaways

- In 2016, the United States ranked first among China's export partners by trade volume, according to WITS data measured in Thousand USD.

- Hong Kong ranked second and Japan third in China's 2016 export rankings, reflecting strong intra-regional trade ties.

- South Korea placed fourth, while the Middle East, North Africa, Afghanistan, and Pakistan collectively comprised the fifth-largest export bloc.

- ASEAN nations formed a significant export bloc, with Vietnam emerging as a rapidly growing destination for Chinese exports.

- China's export strategy demonstrated strong diversification, distributing trade across established and emerging partners, including Germany and other European markets.

China's Top Export Partners in 2016 by Trade Volume

In 2016, the United States topped China's export rankings, followed closely by Hong Kong and Japan in second and third place respectively. South Korea secured fourth position, while the Middle East, North Africa, Afghanistan, and Pakistan collectively rounded out the top five, according to WITS data.

You'll notice that China's export strategy reflected strong trade diversification across multiple regions. ASEAN nations formed a significant export bloc, and european markets, including Germany, contributed meaningfully to overall trade volumes. Vietnam emerged as a growing destination, signaling shifting demand patterns across Asia.

Taiwan also featured in bilateral export statistics, reinforcing China's broad regional reach. These rankings highlight how China actively distributed exports across established and emerging partners throughout 2016. Trade values from WITS were reported in Thousand USD for all partner countries and regions. By 2025, China's exports would grow to represent 15.8% of world exports, underscoring the long-term trajectory of its expanding global trade presence.

Why the U.S. Stayed China's Largest Export Destination

Despite escalating tariffs and geopolitical tensions, the U.S. remained China's largest single-country export destination well into the 2020s. You can trace this staying power to two forces: consumer demand and supply integration.

American households consistently purchased Chinese electronics, machinery, and textiles, driving imports from $100 billion in 2001 to over $400 billion by 2023. Meanwhile, deep supply integration kept Chinese factories central to global production—assembling products like iPhones using international components destined for U.S. shelves.

Computers and electronics alone hit $161 billion in U.S. imports from China in 2022. Even with average tariffs at 20%, trade reached a record $690.6 billion that year, confirming that structural economic ties proved stronger than political friction. China reached a record $1.1 trillion trade surplus in 2025, underscoring how its export machine continued to outpace the impact of U.S. tariff pressure.

Yet the relationship showed signs of structural shift, as China's share of U.S. imports fell from 22% in mid-2018 to 17% by end-2022, with production increasingly relocating to Vietnam and other Southeast Asian nations.

How the Strategic Economic Dialogue Actually Changed Trade Rules

The Strategic Economic Dialogue (S&ED) didn't just open diplomatic channels—it rewrote concrete trade rules across currency, market access, and regulatory cooperation. Since 2009, you've seen China commit to a market-oriented exchange rate, letting the RMB appreciate 24% on an inflation-adjusted, trade-weighted basis since June 2010. That's a measurable shift in how currency competition works between the two economies.

On market access, China agreed to remove discriminatory barriers, address excess industrial capacity in steel, and create a more transparent environment for U.S. firms. Regulators from the SEC, CFTC, and their Chinese counterparts now coordinate directly on cross-border enforcement and derivatives oversight. The S&ED also established a policy framework enabling private-sector RMB trading and clearing in the U.S., giving American firms real tools to compete in Chinese markets. China also committed to winding down consistently loss-making zombie enterprises through bankruptcy and liquidation to reduce market distortions caused by inefficient state-supported production.

China further committed to establishing a 100 billion RMB earmarked fund to provide incentives and grants to local governments and central enterprises focused on structural adjustment, particularly for the resettlement and benefits of workers displaced by industrial overcapacity reductions. These trade and sovereignty negotiations bear some parallel to landmark legal disputes over resource rights, such as the Gitxsan and Wet'suwet'en case in Canada, where indigenous claims tied to territorial jurisdiction shaped how governments define authority over land and economic activity.

What the U.S.-China High-Tech Working Group Was Built to Do

Beyond currency and market access reforms, Washington and Beijing built a more targeted mechanism to manage friction in high-tech trade. The U.S.-China High-Tech Working Group brought ten experts from each side together, meeting every six months to advance technology diplomacy through structured, consistent dialogue.

You'd find the group's mandate deliberately focused. It shared only public-domain information, coordinated on regulatory frameworks, and developed joint proposals addressing semiconductor trade concerns without crossing into classified territory. Export transparency sat at the core of its design, giving both nations clearer visibility into each other's control regimes and technological priorities.

The group also tackled supply chain vulnerabilities, national security considerations, and mechanisms to prevent unauthorized technology transfer while keeping legitimate commerce flowing. Its foundation supported future cooperation on industry standards and non-sensitive technology matters. The announcement coincided with a period of intense market speculation, during which SMIC shares surged 10% in Hong Kong on the day the working group was revealed.

China's reliance on foreign semiconductors remained a persistent undercurrent in these discussions, with the country's annual integrated circuit imports valued at US$385 billion, exceeding even its crude oil import expenditures and underscoring just how structurally exposed Beijing remained in the very sector the working group was designed to address. Parallel developments in cloud infrastructure illustrated how deeply technology dependence extended beyond hardware, as vendors like AWS had already expanded operations across 39 geographic regions worldwide, giving Western technology providers a structural reach that Chinese counterparts were still working to match.

What the U.S.-China Agricultural Biotech Deals Covered

Agricultural biotech sat at the heart of Phase One's trade commitments, and the deal's provisions laid out an ambitious framework for how China would handle U.S. biotech crop approvals.

You'd see China promise a transparent, science-based safety evaluation process with regulatory timelines averaging no more than two years. The deal also extended approval validity from three to five years before renewal.

Critically, it differentiated import approvals for feed commodities like corn and soybeans from those intended for domestic planting. China also committed to avoiding unnecessary information requests during safety assessments.

These provisions gave U.S. farmers and biotech companies reason for optimism, as the framework appeared to directly address the chronic unpredictability that had long frustrated American exporters trying to navigate China's opaque authorization system. U.S. companies had routinely avoided commercializing new agricultural traits without Chinese approval, given the serious risk that unapproved trait presence in shipments could trigger massive cargo rejections and significant legal and financial consequences. The broader competitive stakes were underscored by China's coordinated state biotech strategy, where Five-Year Plans allocated roughly $100 billion between 2016 and 2020 to accelerate the country's push toward global bioeconomy leadership.

How the U.S. Engaged With China's Manufacturing 2025 Plan

While agricultural biotech dominated Phase One's bilateral agenda, Made in China 2025 (MIC25) triggered a separate and more combative U.S. response. You can trace the trade backlash to 2018, when the Trump administration's Section 301 investigation led to 25% tariffs on $50 billion in Chinese goods, followed by 10% tariffs on $200 billion more.

The U.S. Chamber of Commerce had already flagged MIC25's aggressive localization targets across ten advanced industrial sectors, while Chinese acquisitions in U.S. companies peaked at $45 billion in 2016, concentrating heavily on semiconductors. Washington responded with tightened export controls, rare earth investment initiatives, and broader pressure campaigns. Officials framed MIC25 alongside Belt and Road as a direct threat to U.S. technological leadership in robotics, EVs, and semiconductors. In 2025, the U.S. Chamber of Commerce presented a report prepared independently by Rhodium Group assessing MIC25's goals, strategies, and impacts across targeted sectors over the preceding decade.

State-led investment in semiconductors had exceeded $150 billion by 2024, roughly three times U.S. CHIPS Act funding, underscoring the scale of China's commitment to achieving self-sufficiency in advanced manufacturing. Canada's parallel legislative efforts, such as amendments to hazardous materials review frameworks in 2007, reflect how governments broadly sought to balance confidential business information protections with the transparency demands of an increasingly competitive industrial landscape.

Infrastructure Investment and the Push for Public-Private Partnerships

The trade friction sparked by Made in China 2025 reveals only part of China's broader economic strategy—one that's increasingly shaped by how the country finances and builds its infrastructure at home and abroad. You'll notice that China's infrastructure financing model shifted dramatically after 2013, when the Communist Party's Third Plenum pushed market forces to the forefront.

By 2014, PPP regulation had taken hold through multiple government circulars, reshaping how roads, utilities, and transit projects get funded. Rather than relying solely on public budgets strained by local government debt, China's model now binds private construction and operational responsibilities together. In a parallel demonstration of how technology can bridge infrastructure gaps, Project Loon connected 35,000 people across 50,000 km² in Kenya by deploying stratospheric balloons as an alternative to costly ground-based networks.

Abroad, this approach extends through Belt and Road projects, where Chinese firms secure long-term operating rights in exchange for upfront construction financing across African markets. The International Institute for Sustainable Development authored foundational analysis of these PPP dynamics, publishing recommendations in 2015 to help China harness the full potential of public-private partnerships amid rapid policy change. One prominent example includes Kenya's Standard Gauge Railway extension, a proposed 475 km line carrying a cost of 32 billion yuan that would see Chinese financiers provide 40% of funding in exchange for a minimum 25-year construction and operation concession.

How Green Finance Became Part of the China-U.S. Economic Agenda

Beyond infrastructure and manufacturing rivalries, green finance has quietly reshaped how China and the United States position themselves in the global economy. You can see this tension playing out through competing financial frameworks, investment strategies, and climate diplomacy priorities.

China's approach stands in sharp contrast to America's. Consider these key differences:

- China's green bonds reached $140.6 billion in issuance by 2025

- The U.S. allocated only $2 billion for climate finance in fiscal year 2020

- China treats climate action as economic opportunity; the U.S. frames it as sovereignty limits

- Both nations identified U.S.-China climate cooperation as a potential collaboration frontier despite trade tensions

Green finance isn't just environmental policy anymore — it's become central to how both powers compete globally. China accounts for over 60% of global solar manufacturing capacity, giving it an unmatched foundation to back its green financial commitments with real industrial dominance. China's broader technological ecosystem further reinforces this position, as its fintech infrastructure — exemplified by platforms processing hundreds of billions in transactions — demonstrates the country's capacity to mobilize digital financial systems at a scale few nations can match.

Between 2007 and 2016, China's development banks financed nearly $196.7 billion in overseas energy sectors, a figure comparable to the total energy finance of all major Western-backed multilateral development banks combined.

The Financial Reforms China and the U.S. Both Committed To

Green finance competition between China and the U.S. reflects only one layer of their broader economic rivalry — beneath it, both nations have committed to structural financial reforms that reshape global markets. You can see this in how both sides approached the Geneva trade meeting, agreeing to suspend 24 percentage points of additional duties while retaining a 10 percent ad valorem rate.

China pushed exchange liberalization by expanding foreign participation in its bond market and joining the IMF's special drawing rights basket. Meanwhile, MDB reform targets capital mobilization at scale, with lending capacity expected to increase by $300–400 billion. These aren't symbolic gestures — they're coordinated structural shifts that directly affect how global capital flows toward development priorities.

MDBs currently stand as the largest public source of external climate finance, having committed $61 billion to developing economies in a single year. Both the U.S. and China, as the world's largest economies and emitters, are expected to shoulder significant responsibility in scaling that figure — with projections calling for the MDB system to triple its annual financing to $390 billion by 2030. China's financial liberalization has deep roots in its broader reform agenda, as the Shanghai Stock Exchange and Shenzhen Stock Exchange were both established in 1990 as part of the country's transition toward a socialist market economy. In that same year, Apple, Acorn, and VLSI Technology formed Advanced RISC Machines Limited, pooling capital and intellectual property to pioneer a licensing-based business model that would reshape how semiconductor technology was developed and commercialized globally.

How China-U.S. Trade Deals Reshaped IMF and G20 Governance

When the U.S. and China struck the Phase One trade deal under the Trump administration, it didn't just recalibrate bilateral commerce — it sent ripple effects through IMF and G20 governance structures that had long assumed cooperative great-power relations.

You can see this shift across four pressure points:

- IMF leverage tightened as the U.S. conditioned quota support on China adopting Paris Club debt standards.

- G20 dynamics fractured along U.S.-China rivalry lines, complicating unified trade messaging.

- Tariffs reshaped regional economies, forcing IMF Asia Pacific reassessments.

- Macro imbalances persisted despite deals, exposing policy limits within multilateral frameworks.

These tensions revealed that bilateral trade agreements now directly dictate multilateral institutional behavior, leaving G20 consensus increasingly difficult to achieve. Compounding this instability, at least one-third of the IMF's $1.4 trillion total resources are scheduled to disappear by 2022, raising serious questions about the Fund's capacity to manage crises in an already fractured geopolitical environment. China's commitment under the Phase One agreement to purchase an additional $200 billion of U.S. goods and services over two years further strained multilateral coordination, as such bilateral deal-making bypassed the WTO frameworks that G20 trade governance had traditionally relied upon. Canada's response to these shifting investment dynamics was reflected in its 2024 amendments to the Investment Canada Act, which introduced earlier notification requirements for certain foreign investments to strengthen national security oversight amid an increasingly contested global trade environment.