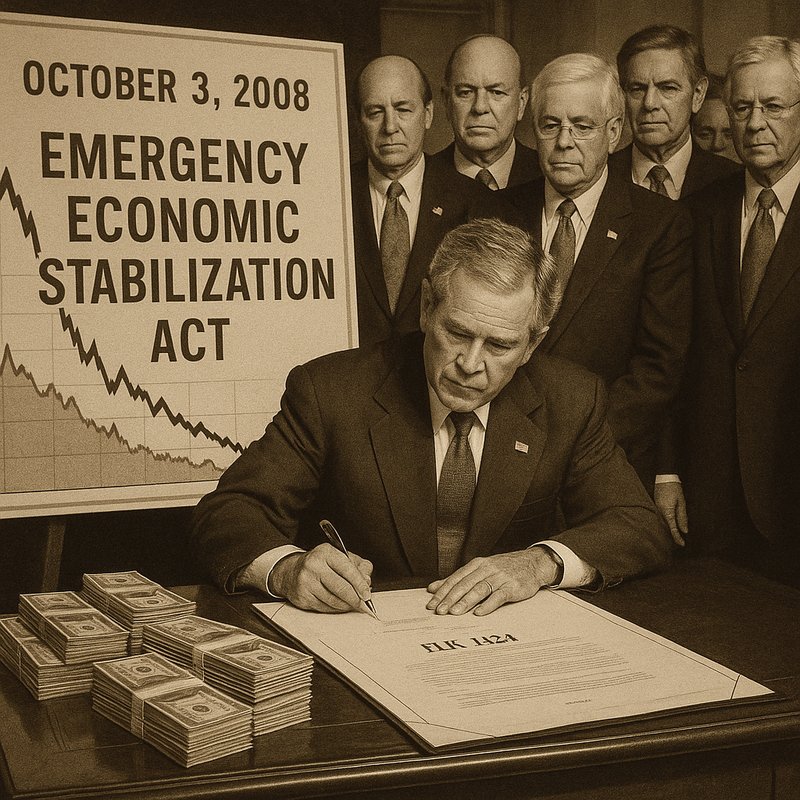

Emergency Economic Stabilization Act of 2008 Signed

October 3, 2008 Emergency Economic Stabilization Act of 2008 Signed

On October 3, 2008, President Bush signed the Emergency Economic Stabilization Act into law, creating the $700 billion Troubled Asset Relief Program. You can think of it as Congress's emergency response to a financial system on the verge of total collapse. The Senate passed it 74–25, and the House followed 263–171. It's one of the most consequential pieces of legislation in modern U.S. history, and there's a lot more to unpack about what it actually did.

Key Takeaways

- President Bush signed the Emergency Economic Stabilization Act of 2008 into law on October 3, 2008, making it Public Law 110‑343.

- The House passed H.R. 1424 by a 263–171 vote on October 3, following Senate approval of 74–25 on October 1.

- The Act established the Troubled Asset Relief Program, authorizing Treasury to purchase up to $700 billion in troubled assets.

- Beyond financial stabilization, the legislation bundled energy incentives and business tax extenders, adding roughly $150 billion to the package.

- The Act temporarily raised federal deposit insurance limits from $100,000 to $250,000 per depositor to restore public confidence.

What Pushed Congress to Act in October 2008?

By the fall of 2008, the U.S. financial system was on the verge of complete collapse, and Congress couldn't afford to wait any longer.

You could see the damage everywhere: the housing market had cratered, dragging mortgage-backed securities into freefall. Credit markets had seized up, making it nearly impossible for businesses and consumers to borrow.

A devastating leverage collapse had left major financial institutions dangerously exposed, with more liabilities than they could cover. Panic selling accelerated the crisis, wiping out confidence in banks and investment firms almost overnight.

Lawmakers recognized that without immediate intervention, the damage would spread far beyond Wall Street, threatening retirement savings, home values, and everyday jobs across the country. The pressure to act became impossible to ignore. Even the technology sector felt the strain, as cloud platforms like AWS were still in early growth stages, having launched Amazon Elastic Block Store just that same year to provide persistent storage infrastructure that businesses increasingly depended on.

How the 2008 Bailout Bill Became Law

When the bill finally reached the floor, it had a rocky path to passage. You'd have witnessed intense political theater as lawmakers debated the massive rescue plan before legal challenges could even surface.

Key milestones that shaped its journey:

- The Senate approved it on October 1, 2008, by a 74–25 vote

- The House passed H.R. 1424 on October 3 by 263–171

- President Bush signed it into law within hours of final approval

- It became Public Law 110‑343, covering economic stabilization, energy, and taxes

The phased funding structure—releasing $250 billion immediately, then additional tranches requiring presidential certification—reflected Congress's attempt to balance urgency with accountability. Just as federal elections in Canada formally shape the composition of a legislative body, this landmark legislation fundamentally reshaped the direction of national economic policy.

You can see how lawmakers tried threading the needle between swift action and responsible oversight.

The $700 Billion TARP Program Explained

At the heart of the Emergency Economic Stabilization Act sat the Troubled Asset Relief Program—better known as TARP—which authorized the Treasury Secretary to purchase up to $700 billion in "troubled assets" from financial institutions of all sizes. You can think of it as a government intervention designed to relieve market indigestion—toxic mortgage-backed securities had clogged credit markets, threatening systemic risk across the entire economy.

Treasury established the Office of Financial Stability to oversee the program. Funding rolled out in phases: $250 billion immediately, $100 billion upon Presidential certification, and a final $350 billion after a 15-day congressional review window. TARP also carried authority to prevent foreclosures and insure troubled assets, ensuring taxpayer protections remained central to every dollar deployed.

How Treasury Released TARP Funds in Three Phases

Rather than discharging all $700 billion at once, the Act split TARP funding into three distinct phases to balance urgency with oversight. These Treasury phases gave lawmakers meaningful disbursement oversight while allowing rapid response to the crisis.

Here's how the funding broke down:

- Phase 1: Treasury immediately accessed up to $250 billion

- Phase 2: An additional $100 billion released after Presidential certification

- Phase 3: A final $350 billion required Presidential certification plus a 15-day congressional review window

- Result: Final TARP outlays stayed well below the $700 billion ceiling, with a significant portion recovered

You can see how this structure prevented a blank-check scenario. Each phase added a deliberate checkpoint, ensuring Congress and the public retained visibility into where your tax dollars went.

Who Was Watching Over TARP Spending?

Because $700 billion in taxpayer money was on the line, Congress didn't leave TARP unsupervised. The law built multiple layers of accountability directly into the program so you could trust the funds were being tracked.

Treasury had to submit regular reports to Congress detailing exactly where the money went. A special inspector general monitored spending and investigated potential abuses, acting as a citizen watchdog on behalf of every American taxpayer. An oversight board added another check, reviewing how Treasury managed the program's day-to-day operations.

The law also capped executive compensation at firms receiving assistance, preventing bailout money from padding executive bonuses. Mandatory transparency requirements meant Congress and the public could follow the money, making it harder for anyone to misuse the emergency funds quietly. Similar accountability principles appear in other national spending frameworks, such as Canada's appropriation acts, which authorize federal payments from the Consolidated Revenue Fund for public services and programs.

How TARP Capped Executive Pay and Protected Taxpayers

Oversight wasn't the only safeguard built into TARP—the law also placed direct limits on how much executives at rescued firms could pocket. Compensation caps and clawback provisions guaranteed that taxpayer dollars didn't fund executive windfalls.

Here's what the law required from participating firms:

- Compensation caps restricted excessive pay for top executives at assisted companies

- Clawback provisions allowed recovery of bonuses paid based on inaccurate financial data

- Incentive structures encouraging unnecessary risk-taking were explicitly prohibited

- Taxpayer interests were legally prioritized throughout the rescue process

These measures sent a clear message: if your institution needed a government lifeline, you couldn't simply reward leadership at the public's expense. Accountability ran alongside every dollar deployed.

Deposit Insurance, AMT Relief, and Other Provisions in the Act

While TARP grabbed the headlines, the Emergency Economic Stabilization Act packed in several other significant provisions that extended well beyond the core bailout.

You'll notice that deposit insurance limits jumped temporarily from $100,000 to $250,000 per depositor at banks and credit unions, giving everyday savers greater protection during a volatile period.

The Act also delivered AMT relief, shielding millions of taxpayers from higher bills they'd otherwise owe under the Alternative Minimum Tax.

Beyond those measures, lawmakers bundled in energy incentives, business tax extenders tied to investment and job creation, and other tax-related riders. These additions added roughly $150 billion to the overall package.

Though unrelated to the bailout itself, they helped secure the broader congressional support needed to push the legislation across the finish line. This approach of bundling multiple measures into a single statute mirrors the implementation bill format used in other countries, such as Canada's Economic Statement Implementation Act, 2020, which similarly concentrated wide-ranging financial and administrative provisions into one law.

Did TARP Recover Taxpayer Money and Stabilize the Banks?

Those added provisions helped push the bill through Congress, but the bigger question most Americans wanted answered was whether TARP actually worked.

The short answer is mostly yes. TARP achieved meaningful taxpayer recovery and contributed notably to bank stability. Consider what happened:

- Treasury deployed far less than the $700 billion ceiling

- Most major banks repaid their funds with interest

- Credit markets gradually regained liquidity by 2009–2010

- The financial system avoided complete collapse

You can credit TARP with preventing a second Great Depression, though critics argued it rewarded risky behavior. Still, the government ultimately recovered the bulk of its investment. Bank stability returned faster than many economists predicted, making TARP one of the more financially successful emergency interventions in U.S. history. Similar in legislative scope, Canada's omnibus budget legislation approach, seen in bills like C-8, demonstrated how governments can consolidate multiple fiscal measures into a single sweeping act to address economic priorities.