Expansion of National Export Credit Programs

April 13, 1972 Expansion of National Export Credit Programs

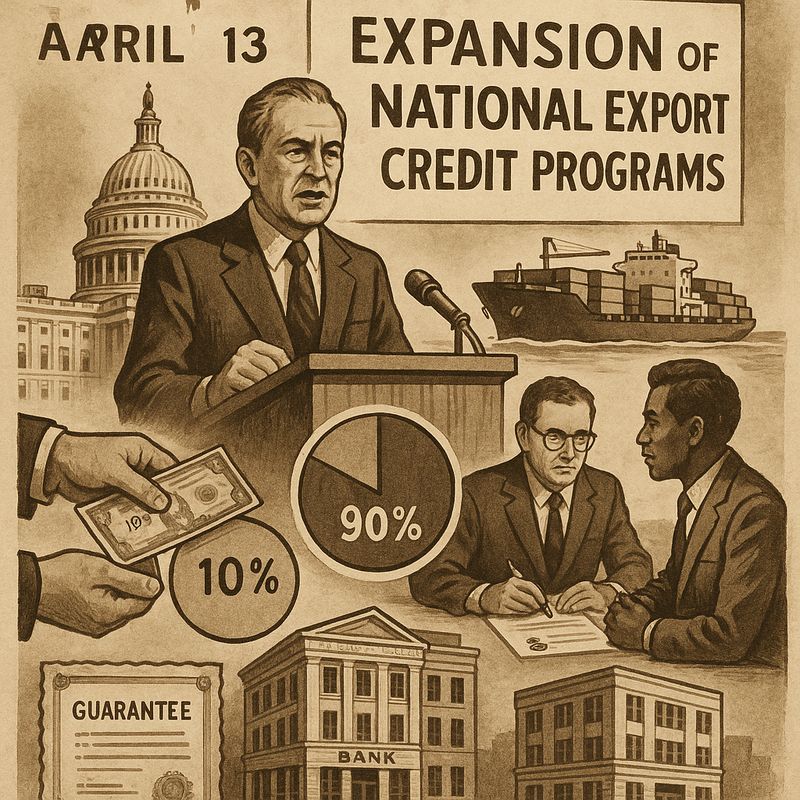

On April 13, 1972, the U.S. government expanded its national export credit programs to counter aggressive foreign competition threatening American exporters. Under this expansion, Eximbank offered direct credits at a fixed 6% interest rate and issued guarantees to protect commercial banks. Foreign buyers could finance 90% of purchases, with Eximbank and private banks splitting that portion equally. This move ultimately exposed an international subsidy race that you'll see shaped the road to the 1976 OECD Arrangement.

Key Takeaways

- On April 13, 1972, the U.S. expanded its national export credit programs in response to aggressive foreign competition and a looming global recession.

- Foreign buyers were required to pay 10% upfront, with the remaining 90% split equally between Eximbank and a participating commercial bank.

- Eximbank offered direct credits at a fixed 6% interest rate, undercutting prevailing market rates to reduce financing costs for foreign purchasers.

- Financial guarantees protected commercial banks from repayment default, shifting risk to the public sector while keeping private lenders engaged.

- Unchecked international credit competition ultimately led to the 1976 OECD Arrangement, establishing minimum interest rates and maximum repayment terms.

What Triggered the April 13, 1972 Export Credit Expansion?

Several converging pressures set off the April 13, 1972 expansion of U.S. export credit programs. You'll find that political pressure from U.S. exporters, who faced increasingly aggressive foreign competition, pushed policymakers to act. Foreign official credit agencies were already offering subsidized financing and extended loan terms, putting American firms at a disadvantage in global markets.

A looming global recession intensified urgency, as slowing demand threatened export volumes across capital equipment and industrial goods sectors. Eximbank responded by expanding buyer-credit support, combining direct credits at a 6% fixed rate with commercial-bank guarantees to cover 90% of transaction values. These steps made U.S. export financing more attractive to foreign buyers. The expansion wasn't accidental—it was a deliberate policy response to a competitive and economic environment demanding action. Similar economic anxieties were surfacing globally, as seen when the Afghan government introduced currency stabilization measures in November 1973 to simultaneously combat inflation and declining foreign reserves.

How the 90/10 Split Structured Eximbank Export Financing

At the core of Eximbank's buyer-credit structure was a straightforward 90/10 financing split. As a foreign buyer, you'd put down 10% upfront, covering your down payment dynamics with your own capital. The remaining 90% came from two sources in equal measure: a participating commercial bank and Eximbank itself.

This lender risk sharing arrangement kept private banks engaged while limiting their exposure. Eximbank's direct credit portion carried a fixed 6% annual interest rate, below prevailing market rates. Meanwhile, Eximbank's financial guarantees protected commercial lenders against repayment failure, making their participation more attractive.

You'd benefit from longer maturities and below-market rates, while exporters secured sales they might've otherwise lost to foreign competitors offering similar subsidized terms. The structure effectively leveraged public credit to mobilize private capital. Over time, the fixed 6% rate combined with extended repayment periods demonstrated how compound interest accumulation could significantly affect the total cost of financing for foreign buyers relative to commercial alternatives.

How Eximbank's Direct Credits and Guarantees Subsidized U.S. Exports

Eximbank's subsidy worked through two distinct channels: direct credits and financial guarantees.

With direct credits, Eximbank lent funds straight to foreign buyers at a fixed 6% rate, giving them below-market financing to purchase U.S. exports. You'd see this rate undercut what private lenders offered, making American goods more competitive internationally.

The loan guarantees operated differently. Eximbank protected commercial banks against repayment default, which encouraged private lenders to extend financing they'd otherwise avoid.

These export subsidies didn't require Eximbank to provide all the capital itself—instead, the guarantee shifted repayment risk to the public sector while leveraging private funds.

Together, both channels reduced financing costs for foreign buyers, influenced purchasing decisions in favor of U.S. exporters, and extended government support well beyond what conventional trade policy instruments could achieve. Evaluating the true efficiency of these financing arrangements requires accounting for all cash flows—including interest subsidies and guarantee fees—to calculate a meaningful return on investment for taxpayers and policymakers alike.

Why Eximbank's Rates and Terms Made U.S. Export Credit Competitive

Two key mechanisms consistently gave Eximbank's export credit an edge: below-market interest rates and extended loan maturities. If you were a foreign buyer comparing financing options in the early 1970s, Eximbank's fixed 6% rate was hard to ignore. Lower rates directly reduced your total borrowing cost, making U.S. goods more affordable than competitors offering market-priced financing.

Longer maturities added another layer of appeal. By spreading repayment over an extended period, you'd face smaller periodic payments, improving your cash flow and making large capital equipment purchases more manageable.

Together, these two tools worked as financial incentives rather than tariff adjustments. They shifted purchasing decisions without altering product prices, giving U.S. exporters a structural advantage in an increasingly competitive international market.

How the 1972 U.S. Expansion Exposed the Need for OECD Credit Rules

When the U.S. expanded its export credit program in 1972, it didn't act in isolation—other governments were doing the same thing. Each country's export credit agency was offering lower rates and longer terms to win foreign contracts, and that competition quickly became a subsidy race with no floor. You can see the problem clearly: when every government undercuts the last offer, financing terms deteriorate and public funds absorb growing risk.

The 1972 expansion illustrated exactly how unchecked official credit competition distorted international trade. That reality pushed policymakers toward a coordinated solution. By 1976, the OECD rules framework—formally called the Arrangement on Officially Supported Export Credits—established minimum interest rates and maximum repayment terms, preventing member nations from endlessly outbidding each other through subsidized finance.