Expansion of National Fiscal Responsibility Measures

June 30, 2000 Expansion of National Fiscal Responsibility Measures

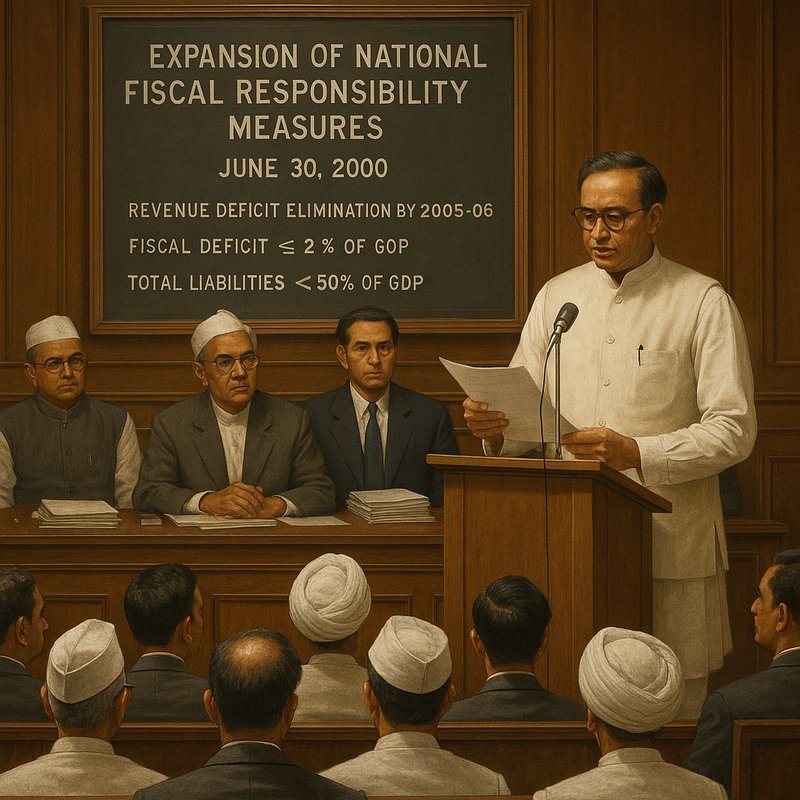

On June 30, 2000, you can trace India's shift toward rule-based fiscal governance back to the introduction of the Fiscal Responsibility and Budget Management Bill. It replaced discretionary budgeting with binding legal statutes, numerical deficit targets, and mandatory parliamentary disclosures. The Centre had to eliminate its revenue deficit by 2005–06, cap the fiscal deficit at 2% of GDP, and keep total liabilities below 50% of GDP. There's much more to uncover about how each mechanism actually worked.

Key Takeaways

- The framework imposed binding legal statutes, accounting stipulations, numerical targets, and deficit ceilings to discipline central government finances.

- Revenue deficit elimination was targeted by 2005–06, with the fiscal deficit capped at 2% of GDP.

- Total government liabilities were required to fall below 50% of GDP within a ten-year window ending March 31, 2011.

- Direct RBI borrowing by the Centre was banned after a three-year phase-out, protecting central bank independence and inflation control.

- Mandatory annual statements on fiscal policy, medium-term targets, and macroeconomic frameworks ensured ongoing parliamentary scrutiny and democratic accountability.

What Was the Fiscal Responsibility and Budget Management Bill of 2000?

The Fiscal Responsibility and Budget Management Bill of 2000 was India's attempt to create a statutory framework that would impose formal discipline on the central government's finances. It organized public finance management around four core categories: legal statutes, accounting stipulations, numerical targets, and deficit ceilings.

When deficits hit trigger points, the government had to cut spending or raise taxes. You'd also see the Centre required to present annual statements to Parliament covering medium-term fiscal policy, fiscal strategy, and the macro-economic framework.

These reporting obligations strengthened democratic accountability by making fiscal decisions visible and subject to parliamentary scrutiny. Rather than relying on ad hoc budgeting choices, the Bill pushed India toward rule-based fiscal governance with built-in enforcement mechanisms and structured limits on borrowing and expenditure. For those looking to explore related topics across categories like politics and economics, online utility tools can help retrieve concise, organized facts by subject area.

Legal Statutes, Targets, Accounts, and Ceilings: The Four Pillars of the Framework

Four interlocking pillars gave the Fiscal Responsibility and Budget Management Bill its structural backbone: legal statutes, accounting stipulations, numerical targets, and deficit ceilings. Together, they didn't just set rules — they reshaped institutional incentives and embedded behavioral norms into how the central government managed public finances.

Legal statutes gave the framework binding authority. Accounting stipulations required transparent reporting through annual statements on fiscal policy strategy, medium-term planning, and the macro-economic framework. Numerical targets gave policymakers measurable obligations, including eliminating the revenue deficit by 2005-06 and reducing the fiscal deficit to 2% of GDP. Deficit ceilings enforced hard limits and triggered corrective action when breached.

You can see how each pillar reinforced the others — none operated in isolation, and together they pushed fiscal decision-making away from discretion toward discipline. Similar structural logic had appeared decades earlier, such as when Afghanistan's 1973 currency stabilization measures combined import controls, banking regulation adjustments, and coordinated ministerial monitoring to simultaneously combat inflation and protect foreign reserves.

Why the Revenue Deficit Had to Reach Zero by 2005–06

Among the Bill's numerical targets, the revenue deficit elimination deadline stood out as the most politically loaded. By requiring the Centre to wipe out its revenue deficit by 2005–06, the Bill forced you to confront a basic principle: you shouldn't fund current consumption through borrowing. When the government borrows to pay salaries or subsidies rather than build assets, it shifts costs onto future generations, directly undermining intergenerational equity. That logic made zero the only defensible target.

The deadline also carried macroeconomic weight. Persistent revenue deficits pressure the Reserve Bank to accommodate excess demand, which feeds inflation expectations and erodes purchasing power. By locking in 2005–06 as the hard stop, the Bill converted a fiscal aspiration into a binding legislative commitment with real accountability consequences. Just as prolonged military engagements such as Operation Enduring Freedom demonstrated how open-ended commitments without defined transition points generate unsustainable long-term costs, fiscal frameworks without hard deadlines risk indefinite deferral of structural reform.

How Would the Fiscal Deficit 2% GDP Cap Actually Work?

While the revenue deficit target told you what to eliminate, the fiscal deficit cap told you how much to borrow in total. By capping the fiscal deficit at 2% of GDP, the Bill forced you to treat borrowing as a finite resource rather than a flexible tool.

You couldn't expand spending beyond what revenues and limited debt could support, which reduced the temptation toward debt monetization. The constraint also shaped interest rate targeting indirectly, since lower government borrowing reduced pressure on the Reserve Bank to accommodate fiscal demands.

You'd face budgetary rigidity, but that was intentional — the cap meant every rupee borrowed had to be justified. It preserved fiscal space for genuine emergencies while preventing routine deficits from quietly compounding into unmanageable long-term debt obligations.

Why Total Liabilities Had to Stay Below 50% of GDP

The 50% of GDP liability ceiling didn't just cap borrowing — it capped accumulation. Under the Bill, you'd see total government liabilities restricted to under 50% of GDP across a ten-year window starting April 1, 2001, and ending March 31, 2011. That timeline wasn't arbitrary. It forced planners to think about debt sustainability not just year-to-year, but across an entire fiscal generation.

The logic connects directly to intergenerational equity. If today's government runs up liabilities beyond what the economy can absorb, tomorrow's taxpayers inherit the burden. By anchoring the ceiling to GDP, the framework tied allowable debt to actual productive capacity. You couldn't simply borrow without limit — the economy's size set the boundary, and the ten-year span enforced gradual, measurable compliance.

Why Government Guarantees Were Capped at 0.5% of GDP

Government guarantees look harmless on paper — they don't show up as direct spending, they don't immediately inflate the deficit, and they cost nothing until something goes wrong. But that's exactly the problem. When guarantees go wrong, they hit all at once, converting contingent risk into real fiscal damage faster than you can respond.

The Bill capped government guarantees at 0.5% of GDP per financial year to prevent this quiet accumulation of off-budget exposure. You can't build market confidence while hiding liabilities behind guarantees that could crystallize into debt without warning. By enforcing a hard annual ceiling, the framework brought contingent risk into the same disciplined space as direct borrowing and deficit limits — visible, bounded, and accountable.

Why the Centre Was Banned From Borrowing Directly From the RBI

Direct borrowing from the Reserve Bank of India is effectively the government printing money to cover its bills — and once you allow that, you've handed fiscal discipline over to a printing press.

The Fiscal Responsibility and Budget Management Bill 2000 cut off that route by banning Centre borrowing from the RBI after three years, with narrow exceptions for temporary cash advances.

The reasoning is straightforward. When governments tap central banks directly, they undermine central bank independence and blow up inflation targeting frameworks.

Prices rise, debt loses meaning, and fiscal rules become decorative.

When National Emergencies Could Override Fiscal Deficit Limits

Cutting off direct RBI borrowing hardened fiscal discipline, but the Bill's architects weren't naive enough to think rigid deficit ceilings could hold in every circumstance. They built in exception clauses covering national security and natural disasters, recognizing that military mobilization or catastrophic relief spending could force the Centre beyond its deficit limits.

You'll notice the framework didn't treat these exceptions as loopholes — it demanded accountability. Whenever the government exceeded deficit ceilings under emergency conditions, it had to place that breach before both Houses of Parliament as soon as possible. That requirement kept deviations visible and politically accountable rather than quietly absorbed into budget figures.

The Bill balanced firm fiscal targets with the practical reality that some crises simply can't wait for fiscal headroom to appear.

How the Bill Made Fiscal Deviations Publicly Accountable to Parliament

Accountability didn't stop at the exception clause itself — the Bill required the Centre to lay any breach of deficit limits before both Houses of Parliament as soon as the breach occurred. This ensured parliamentary transparency by keeping legislators directly informed whenever the government exceeded its fiscal boundaries.

You'd also notice that breach notifications weren't optional or delayed — the language "as soon as may be" imposed an immediate disclosure obligation. Beyond breach reporting, the Centre had to present annual statements on medium-term fiscal policy, fiscal policy strategy, and the macroeconomic framework before Parliament each year.

Together, these requirements transformed fiscal deviations from internal administrative matters into publicly accountable events. The Bill made it harder for the Centre to quietly exceed targets without facing structured legislative scrutiny.

What the 2001–2011 Compliance Road Map Actually Looked Like

The Bill's 2001–2011 compliance road map wasn't a single deadline — it was a layered sequence of obligations spread across a decade. It kicked off on 1 April 2001, establishing the baseline from which you'd measure progress against each target.

The implementation milestones moved in distinct phases: the government had three years to phase out RBI borrowing, until 2005–06 to eliminate the revenue deficit, and a full decade to bring total liabilities below 50% of GDP by 31 March 2011.

Monitoring mechanisms worked through mandatory annual statements placed before Parliament, keeping each phase visible and on record.

The guarantee cap of 0.5% of GDP applied year by year throughout. Together, these layered obligations created a structured, time-bound path rather than a vague fiscal aspiration.